About two-thirds of Millennials and Gen Xers would talk to a financial professional about how to use other income streams to delay filing for Social Security benefits until full retirement age.

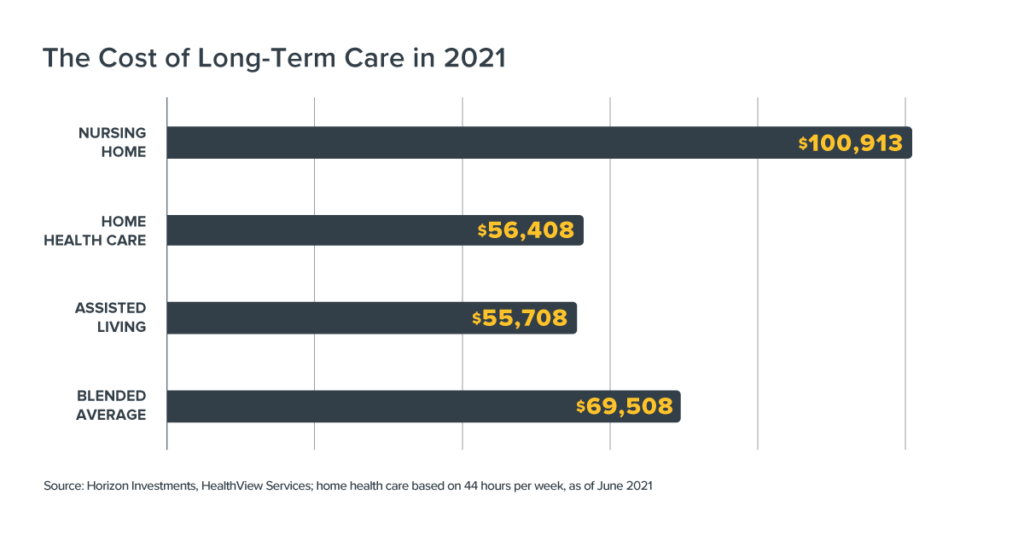

The march higher in the cost of home health, assisted living or nursing home services continues. The blended cost of providing a year’s worth of long-term care is roughly equal to the price of a new Porsche Boxster sports car: $69,508.1

That’s a cost that either has to be covered by someone’s savings and assets, or an insurance policy. Government programs generally are of little help. Medicaid generally doesn’t cover the cost, while Medicare benefits are limited to retirees who have little, if any, assets. (related Big Number: Americans Seek Advice Amid Social Security’s Financial Stress)

(related Big Number: Americans Seek Advice Amid Social Security’s Financial Stress)

For goals-based advisors, the cost of long-term care services may provide another impetus to address longevity risks with their clients.

No matter how fit and healthy retirees work to be with the hope of avoiding major medical issues, on average they still face a good probability of hiring someone to take care of them for an extended period of time.

For example, a 65-year-old female, in good health, has a 56% chance of one day needing long-term care, according to HealthView Services. The probability for a healthy man is 44%.

However, before plugging a long-term care cost estimate into a financial plan, advisors may be well-served by asking clients: “how would you rate your own health?”

The Center for Retirement Research at Boston College found that there’s a “strong relationship’’ between the quality of a client’s self-reported health at age 65-70 and the care they eventually require.2

According to their research, 82% of people who said they were in “fair/poor’’ health subsequently had a moderate to severe need for long-term services and support. Among those who were in“excellent/very good’’ health, just 47% had a moderate to severe need.

(related Big Number: It’s Getting Harder to Fund Retirement Using Bonds)

It is a core belief at Horizon Investments that the most important risk people face in retirement is outliving their money. The rising cost of many things – with health care as a contributing source of retiree inflation – makes it critical, we believe, for goals-based investment managers such as ourselves to design ways to help advisors and their clients grow their assets during retirement with the aim of reducing longevity risk.

(Read Horizon’s Redefining Risk paper to understand our goals-based investing philosophy)

We believe Horizon Investments’ Real Spend retirement income strategy may be helpful as it was designed specifically with the aim of reducing longevity risk. It carries a greater exposure to equities, albeit with risk mitigation, than typically found in traditional financial advice with the aim of providing for necessary distributions, while also aiming to produce stable or growing assets over time.

(related Big Number: Over 65 Years Old and Working? That’s Not as Common Anymore)

See our Real Spend strategy and download our distribution stage brochure for further details about how advisors can help their clients tackle common retirement income challenges, including the cost of long-term care.

To download a copy of this commentary, click the button below.