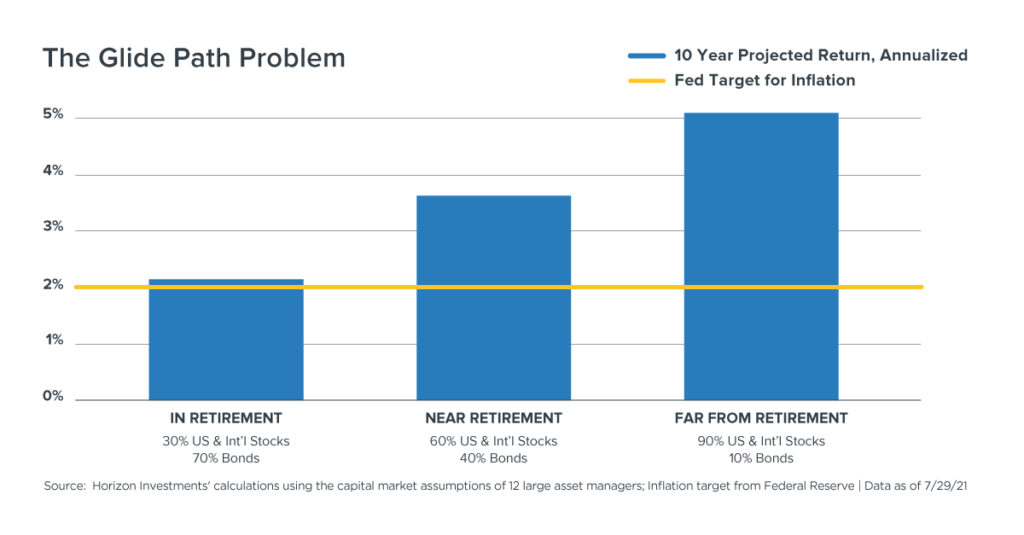

Target date funds that have reached the end of their glide path and have a 30% stocks, 70% bonds allocation may produce essentially no return on an inflation-adjusted basis over the next ten years.

Target date funds operate under the assumption that someone’s asset allocation should follow a glide path, automatically shifting a portfolio to favor bonds over stocks as a person gets closer to their expected year of retirement.

The rationale for offering target date funds is presumably altruistic: help investors facing a long retirement to avoid investment mistakes that may deplete their nest egg.

However, the inflexible nature of the glide path’s embrace of bonds could reintroduce short-fall risk if fixed-income returns are too small to materially make up for account withdrawals and the expected rising cost of living.

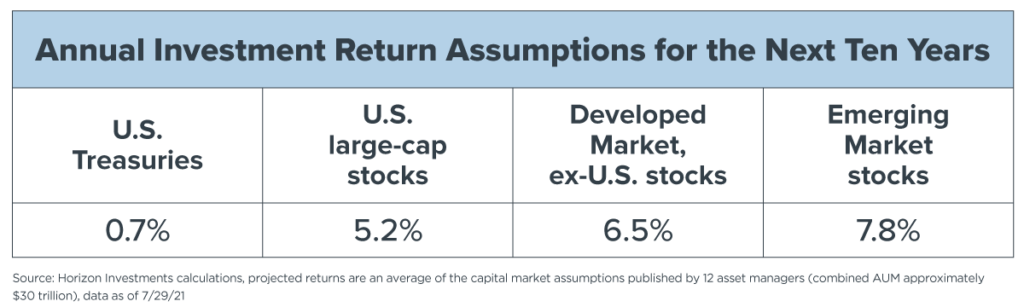

In examining the potential for that risk, Horizon Investments followed a two-step process. First, we collected the projected ten-year returns for global markets published by 12 of the leading investment managers in the industry – the average of their projections is detailed below. Using these projections, and three representative portfolio allocations found in a typical target date fund glide path, Horizon then calculated annualized returns for people who are:

Using these projections, and three representative portfolio allocations found in a typical target date fund glide path, Horizon then calculated annualized returns for people who are:

- Far from retiring with a mix of 90% stocks, 10% bonds

- Nearing retirement with a mix of 60% stocks, 40% bonds

- In retirement with a mix of 30% stocks, 70% bonds1

Based on industry forecasts, retirees with money in a target date fund that’s reached the end of its glide path is expected to produce an average annual return of essentially 0% for the next decade when factoring in the Federal Reserve’s quest to target an inflation rate of 2%. (Note: a retiree’s annual rate of inflation may exceed the Fed’s 2% target. For example, healthcare costs alone are projected to rise by 5.9% per year during a 25-year retirement, according to Healthview Services.2)

Based on industry forecasts, retirees with money in a target date fund that’s reached the end of its glide path is expected to produce an average annual return of essentially 0% for the next decade when factoring in the Federal Reserve’s quest to target an inflation rate of 2%. (Note: a retiree’s annual rate of inflation may exceed the Fed’s 2% target. For example, healthcare costs alone are projected to rise by 5.9% per year during a 25-year retirement, according to Healthview Services.2)

Horizon, as a goals-based investment manager that utilizes active portfolio strategies, believes financial planning in a low-yield world should proactively seek to offset the potentially corrosive impact of both historically small bond yields and rising inflation as a retiree pursues their objectives for current income and legacy wealth.

We also believe that advisors may want to take an active approach to managing those parts of a client’s portfolio that involve glide path strategies given the potential short-fall risks (see our Q2 FOCUS magazine article on active financial advice being the new reality).

Horizon believes that advisors and their clients may want to consider active fixed-income investment management, bond-like alternatives and a larger tilt towards equities to provide the income and growth that today’s retirees will likely need over the course of a long retirement. See the Real Spend® product page for details on Horizon’s distribution strategies that seek to address both short-fall and longevity risks.

To download a copy of this commentary, click the button below.