About two-thirds of Millennials and Gen Xers would talk to a financial professional about how to use other income streams to delay filing for Social Security benefits until full retirement age.

American workers just got another jolt of bad news about the financial health of Social Security. A recent report moved up the program’s insolvency date – when it would have to cut benefit payments – to 2034.1

That’s just 13 years away. It could be a cold splash of reality for mid- to late-career workers who were assuming Social Security would be their main source of retirement income. They may now be more open to professional advice, according to a Nationwide Retirement Institute survey.2

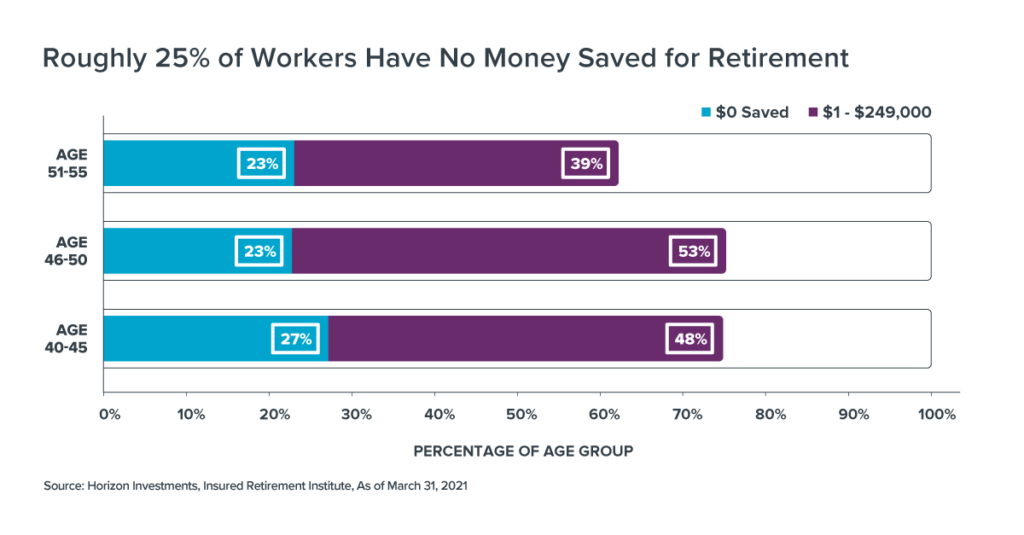

71% of Millennials (aged 25-40) and 70% of Gen Xers (aged 41-56) responded that they’re interested in talking to a financial professional about how to use different income streams with the aim of putting off taking benefits until their full retirement age, when payouts are higher. A separate survey from the Insured Retirement Institute suggests many workers aged 40 to 55 might want to seek professional help, as about 25% of them have nothing saved for retirement.

A separate survey from the Insured Retirement Institute suggests many workers aged 40 to 55 might want to seek professional help, as about 25% of them have nothing saved for retirement.

What looks like a dire problem – a nest egg that’s too small, the possibility of reduced Social Security benefits, and retirement investing options that become more conservative over time – doesn’t have to become a desperate situation.

Our answer in this situation is to use goals-based financial planning and investing.

In a goals-based framework, the primary retirement risk is longevity – or outliving one’s money – a risk that likely hits close to home for people with limited savings. That existential concern is likely more important to people nearing retirement than the traditional view that focuses on reducing portfolio volatility as someone gets older.

Reorienting to longevity, then, causes a fundamental change in the objective of the retirement plan for people with limited savings: determine how to produce sufficient investment returns to sustain a nest egg for as long as possible, while also supporting a payout ratio that takes the threat of reduced benefits into consideration.

(Read Horizon’s Redefining Risk paper to understand our goals-based investing philosophy)

Horizon Investments’ Real Spend retirement income strategy may be helpful as it was designed specifically with the aim of reducing longevity risk. It carries a greater exposure to equities than what is typically found in traditional financial advice or target date funds with the aim of producing stable or growing assets over time.

The Real Spend equity allocation decisions, coupled with tactical risk mitigation and an intelligent rebalance design, are designed with the goal of limiting a retiree’s investing risk in meeting their pressing short- and long-term financial needs.

See our Real Spend strategy and download our distribution stage brochure for further details about how advisors can help their clients tackle common retirement income challenges, including Social Security.

To download a copy of this commentary, click the button below.