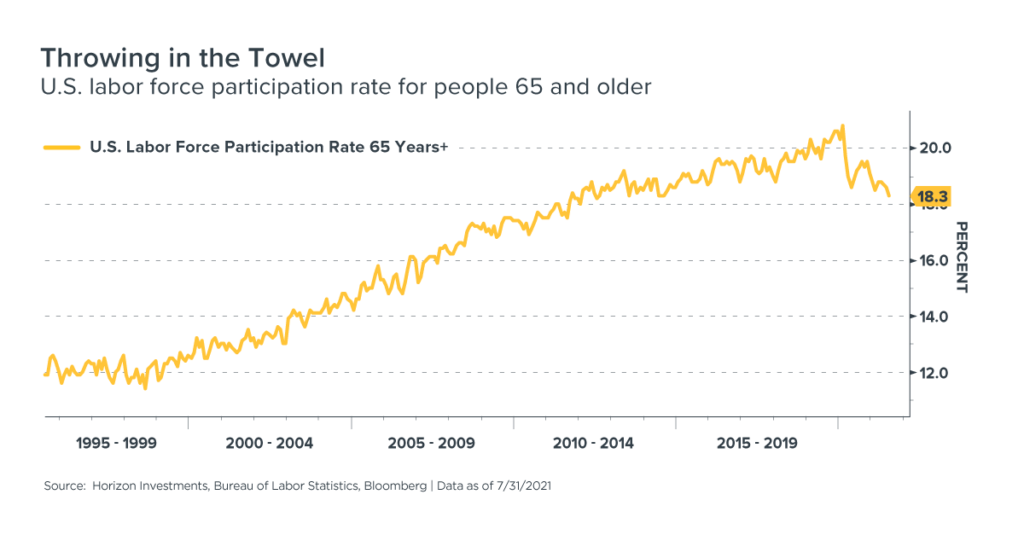

The long-term trend of more people working past the age of 65 may be over; that group’s labor participation rate sank to a seven-year low of 18.3% last month.

The Baby Boomer retirement wave, sparked by Covid, rolls on. Another 248,000 Americans over the age of 65 left the labor force last month, according to the July employment report released last Friday.1

Since the economy was shut down in March last year, 3.16 million people have given up on the idea of working past the typical retirement age, according to Bureau of Labor Statistics data. That cut the labor force participation rate for people aged 65 and over to a seven-year low of 18.3%, potentially ending a two-decade uptrend. The exodus of people aged 65 and over from the job market partially explains why companies are having trouble finding workers as the economy rebounds.

The exodus of people aged 65 and over from the job market partially explains why companies are having trouble finding workers as the economy rebounds.

Older workers may be convinced that a surge in the value of their retirement accounts gives them the financial firepower to exit the workforce. The average 401(k) account balance for those 65 and older leaped by 18% last year to $255,151, according to Vanguard’s long-running series titled “How America Saves.”2 Presumably, this year’s U.S. stock market rally to all-time highs is adding to that retirement savings.

However, many other Americans have too little saved for retirement. And their goal was to extend their working lives so they could delay taking Social Security benefits.

Remember that women have a 31% probability of living to age 95 if they’re in excellent health at age 65; the probability for men in excellent health is 21%, according to the Society of Actuaries.3

Retirees could also face the possibility of shortfall risk if their portfolio is too heavily allocated to traditional bonds during a time of historically low yields. A recent Big Number report said the inflation-adjusted, ten-year return on a portfolio of 30% stocks and 70% bonds could be zero over the next decade, based on the capital market return assumptions from 12 leading investment firms.

Horizon believes a potential solution for the longevity and shortfall risks retirees face is its Real Spend® strategy. It can offer retirees a comprehensive distribution plan designed to meet their goals of steady income, preserving savings and growing assets during what could be a three-decade retirement. And as we detailed in an April Big Number report, financial advisors can choose a higher Real Spend® distribution rate to serve as primary income for clients who are speeding up their retirement timeline, and later switch to a lower payout rate for supplemental income.

To download a copy of this commentary, click the button below.