Number of Americans aged 55 and over applying earlier than they expected for Social Security due to the pandemic

Millions of workers are retiring early. But not necessarily because they want to. The pandemic is pushing them to bow out of a job, according to the Census Bureau.

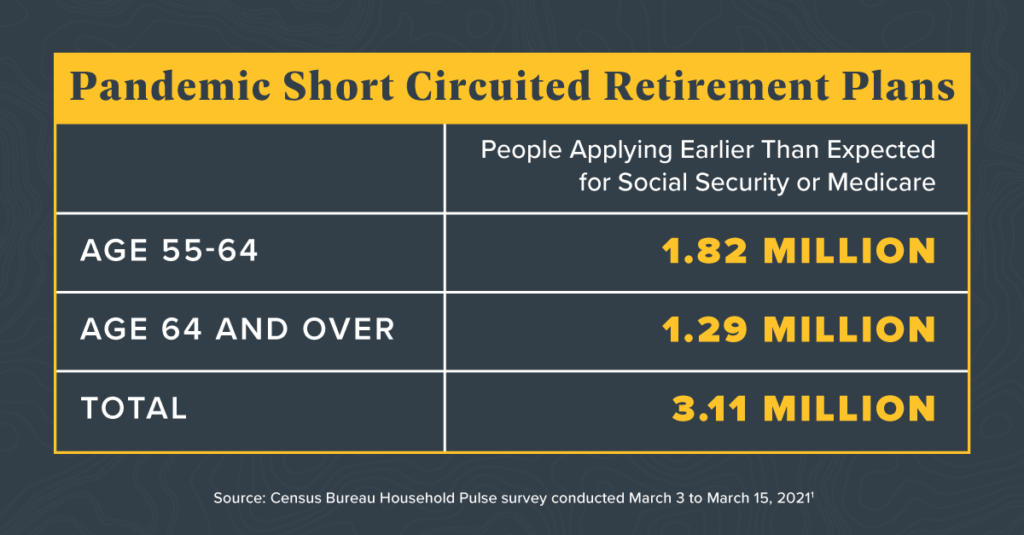

3.1 million Americans aged 55 and over say they’ve applied for Social Security earlier than they were expecting due to COVID-19, according to a Household Pulse survey conducted last month. Of that group, 1.8 million are 55 to 64 years old, meaning they’re too young to receive full retirement benefits from the government-run program.

Retiring early can pose difficult household budget questions. For example, deciding to take Social Security before full-retirement age means a lower monthly check for the rest of a person’s life and would affect a spouse’s benefit should they become a widower. (See our Big Number report on poverty risk for widows.) It also cuts short the time spent saving, investing and reaping compounded returns that are needed to fund retirements that are becoming longer.

Someone considering early retirement should be aware that there’s a reasonably good chance they could live for 35 more years. The Society of Actuaries’ Longevity Illustrator calculates that men and women currently aged 55 – retired, in excellent health and non-smokers – have a 43% and a 53% probability, respectively, of reaching age 90.

Outliving your money – or longevity risk – is something Horizon Investments views as one of the greatest dangers for people in the distribution phase of their investment journey. And that’s especially true for someone who’s retiring early.

To solve for longevity risk, our goals-based financial planning research shows a broad exposure to equities is needed to keep up with a rising, inflation-adjusted cost of living. However, with more stock market exposure comes the possibility of a drop in value. Therefore, we believe a portfolio needs to protect against that with a built-in shock absorber.

Horizon believes the design of its Real Spend® product meets those needs and could help people prematurely leaving the workforce to achieve their financial planning goals.

For example, early retirees who want to delay taking Social Security can start with a higher Real Spend® distribution rate that is designed to serve, initially, as a primary source of income. And then, when government benefits begin, they can switch to a Real Spend® portfolio with a lower payout rate for supplemental income, while also seeking to grow their investment nest egg so it lasts for decades to come.

1 https://www2.census.gov/programs-surveys/demo/tables/hhp/2021/wk26/socsec3_week26.xlsx

2 https://www.longevityillustrator.org/

To download a copy of this commentary, click the button below.

Further reading:

Widows Are at Higher Risk of Falling Into Poverty

Many Investors Tried to Trade the Pandemic Plunge in Stocks

Are Bonds in a Bear Market? That’s the Wrong Question to Ask

If Inflation Returns, Bond’s Diversification Power May Disappear

Essentially Nothing. That’s How Much Bonds May Return Over Next Five Years

It’s Getting Harder to Fund Retirement Using Bonds

Is Now the Time for ESG? Download the White Paper

7.9 Trillion Reasons Not to Fight the Fed, ECB, BOJ or BOE

This commentary is written by Horizon Investments’ asset management team. For additional commentary and media interviews, please reach out to Chief Investment Officer Scott Ladner at 704-919-3602 or sladner@horizoninvestments.com.

To discuss how we can empower you please contact us at 866.371.2399 ext. 202 or info@horizoninvestments.com.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments. Index information is intended to be indicative of broad market conditions. The performance of an unmanaged index is not indicative of the performance of any particular investment. It is not possible to invest directly in an index.

Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent.

The Real Spend® retirement income strategy is NOT A GUARANTEE against market loss and there is no guarantee that the Real Spend® strategy chosen by an investor will be successful for the entirety of an investor’s retirement. Clients may lose money. Real Spend® is an asset allocation strategy that uses an investment model to (i) plan savings amounts and overall asset allocation during the distribution phase of retirement planning, (ii) compute target retirement wealth, assuming a retirement budget and a spending-investment strategy after retirement, (iii) compute the transition from the accumulation phase to the retirement phase, and (iv) generate the spending-investment strategy after retirement. Our retirement spending investment strategy uses an allocation model that replenishes cash needed for withdrawals. Before investing, consider the investment objectives, risks, charges, and expenses of the strategy. All investing involves risk. This strategy is not an insurance product with payments guaranteed. It is a strategy that invests in marketable securities, any of which may fluctuate in value. There is a possibility of outliving the assets if market performance is lower than forecasts used in planning, or if longevity is longer than anticipated. Investors should note that historical data suggests that higher Spend Rates will have a lower likelihood of success for the entirety of the retirement period than a lower Spend Rate would. Past performance and market data are no guarantee of future results and investor experiences will vary.

Other disclosure information is available at hinubrand.wpengine.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2021 Horizon Investments LLC