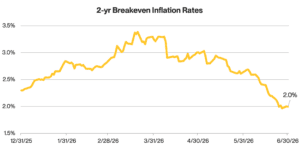

As we highlighted last quarter, the oil price and supply shock impacts from the War in Iran should range from minimal to moderate if the time under conflict is brief – and that is exactly what we got. While passage through the Strait of Hormuz has not fully normalized, the disruption is manageable. Both sides have made progress towards a resolution, giving markets the green light to look beyond negative headlines. Chart 1 shows this through breakeven inflation rates implied by the Treasury Inflation-Protected Security (TIPS) market, where two-year breakeven rates now sit at 2% from a peak of nearly 3.4%, and are surprisingly lower than where we started the year.

Chart 1: Expected Inflation Has Abated

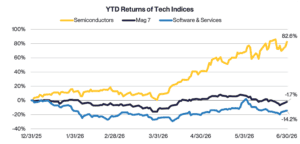

A broadening among stocks in recent years has generally been associated with underperformance among the Magnificent 7 and the largest-cap companies. The second quarter, however, told a different story. Rather than broadening, market leadership narrowed around AI infrastructure, driving significant disruption within the Technology sector. For the first time in many years, we’ve seen persistent weakness among the Magnificent 7. Not because leadership broadened, but because it shifted to a different, still narrow, group of AI beneficiaries. Chart 2 illustrates this rotation following the semiconductor sector’s best quarter on record. As a group, the Magnificent 7 posted a small loss through the second quarter, while the software space has only barely recovered from a disastrous first quarter amid fears AI could make most of the sector obsolete.

Chart 2: Disruption Among Technology Segments

Despite concerns that AI has inflated a market bubble, we believe the opposite has actually happened. Stock prices have risen, but earnings have risen even faster, leaving valuations down nearly 10% for the year in large-cap U.S. stocks. Markets aren’t getting more expensive. They’re getting more profitable.

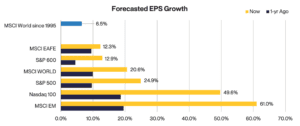

Chart 3 shows earnings growth clearly across major global market segments. Looking back over the past 30 years, global stock earnings growth averaged about 6.5%. Today, however, we see global earnings growth at over 20%, with an inflection higher across all major markets from already-elevated levels one year ago.

Chart 3: Earnings Growth Has Exploded

Key Takeaways

As we look to the second half of the year, we think focus will shift from navigating geopolitical uncertainty to evaluating how policy, innovation, and capital markets evolve around these broad themes:

- Inflation risk has receded, but will it last? We believe so and will look to a committed Fed under new leadership to follow through and allow markets to focus more on economic fundamentals.

- AI has entered a new phase of leadership and has finally broadened beyond the hyperscalers. Looking ahead, the next stage of AI may shift from building infrastructure to generating measurable productivity gains and earnings growth across a much wider range of industries.

- Earnings are in the driver’s seat. Identifying the market segments poised for accelerated operating leverage from AI-driven productivity gains is likely the next wave of disruption.

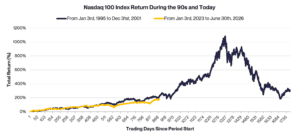

Chart 4: The 90s vs. Today