In the wake of the U.S.-Israeli attacks on Iran and the resulting on-again/off-again shutdown of the Strait of Hormuz, oil prices soared from $57 per barrel at the start of the year to $110 by the end of March. These developments left some concerned about a 1970s-style gas crisis and runaway inflation.

This oil price and supply shock is in no way helpful to the prospects for economic growth, consumer confidence, or inflation. But the extent of the harm will greatly depend on what we’re calling time under conflict. The impact will likely range from minimal to moderate if the disruption is relatively brief, whereas a longer conflict will cause greater economic damage.

With that said, the energy landscape (particularly in the U.S.) has significantly changed over the past 50 years, and the economy and consumers are in a much stronger position to weather this storm:

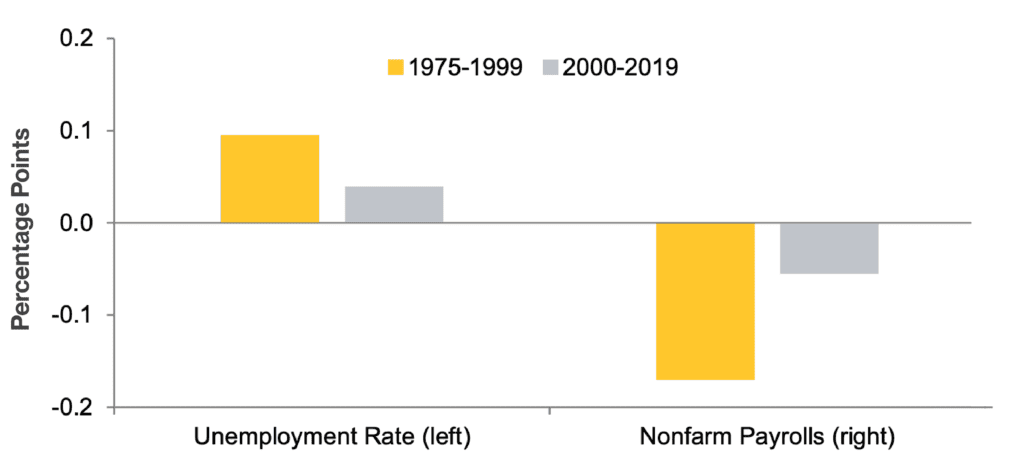

- The economy and labor market are much more insulated from energy and oil price shocks than they used to be: As seen in Exhibit 1, a 10% increase in oil prices has been far less harmful to the employment rate in recent decades than it was during the late twentieth century. One key reason is that the economy’s “energy intensity” is far lower than it’s ever been, meaning it takes much less energy to produce each unit of economic output.

Exhibit 1: Effect of 10% Increase in Oil Prices on U.S. Labor Market (1 Year After the Increase)

- Consumers spend less on energy: U.S. consumers spend far less on energy today as a percentage of their incomes than they did back in the 1970s and 1980s (see Exhibit 2).

Exhibit 2: U.S. Consumer Spending on Energy (As a Percentage of Income)

Despite a turbulent geopolitical backdrop, U.S. equity markets opened 2026 on a solid footing, with the S&P 500 posting a 1.3% gain in January. That resilience was no coincidence, as the U.S. economy started the year from a position of notable strength, capping three consecutive years of exceptional equity market performance with a 17.9% return in 2025.

One key pillar of that resilience is the American consumer. Workers’ wages continue to grow faster than inflation, giving them more purchasing power and helping provide greater financial stability.

That said, even before the conflict in Iran began, there were signs of softening in the labor market. Of note, the average number of jobs created over the last six months is about 15,000, while at the end of 2024, that figure was 104,000. Despite the extreme volatility in month-over-month figures, the trend toward a cooling labor market is clear in the data.

The result is what’s described as a “low hire/low fire” environment, in which companies are reluctant to add workers yet equally hesitant to let existing ones go – leading to a decline in net job creation that has not been accompanied by a meaningful increase in the unemployment rate (see Exhibit 3).

Exhibit 3: Six-Month Moving Average for Nonfarm Payrolls

Recent private credit headlines have been sensational enough to make en masse investor redemption requests seem rational. Terms like “catastrophe,” “crisis,” and “meltdown” are thrown around freely – pouring fuel on what is, in our view, a small fire.

Taking a step back (or several), private credit refers to business loans issued by institutions other than banks or publicly issued bonds. As banks retreated from high-risk lending after the 2008-2009 financial crisis, hedge funds, pension funds, and other large institutions moved in, helping the private credit market grow from $46 billion in 2000 to around an anticipated $2 trillion by 2026. More recently, cracks have appeared, particularly among software borrowers facing disruption from AI.

That pressure has rattled investors, with some rushing to redeem, only to run into the structural reality of private credit: limited liquidity. Cue 2008 echoes: illiquidity and opacity.

While losses are possible if defaults rise, we believe the current stress is unlikely to pose a systemic risk for two primary reasons:

- Size: Despite private credit’s rapid growth, it remains a relatively small component of the overall lending market. Private credit, as a percentage of households’ and businesses’ total loans and debt, remains a small share of private-sector debt, as shown in Exhibit 4 below.

Exhibit 4: Private Credit Remains a Small Percentage of all U.S. Private Sector Debt