Equity investors should look beyond the usual suspects these days

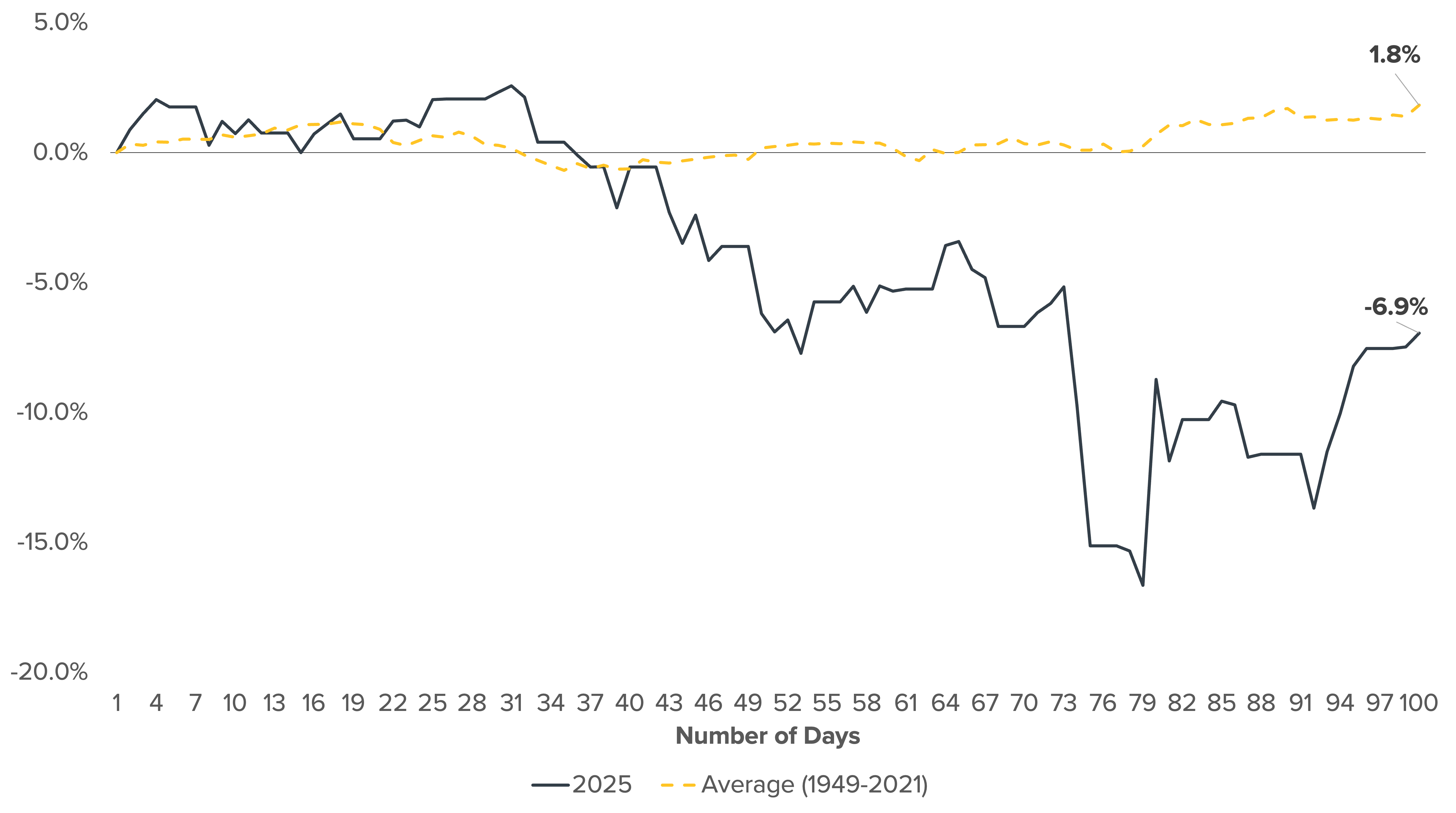

This week marks the 100th day of President Trump’s current term in the White House. And while it’s not the absolute worst 100-day post-inaugural period for U.S. stocks in history, it’s awfully close.

Case in point: The S&P 500 has fallen 6.9% since Trump took office on January 20 (see the chart). The only year investors saw a worse first-100-day return was 1972, when stocks were down nearly 10%. Over the long term, the index has averaged a 1.8% gain during this period.

Meanwhile, the once-red-hot Magnificent 7 stocks have collectively declined by almost 17% since the inauguration.

S&P 500’s Return Over First 100 Days of Presidential Term: 2025 Versus Long-Term Average

Source: Bloomberg, calculations by Horizon Investments, data as of 04/29/2025.

The stock market delivered better-than-average returns to investors both immediately after the election and during the early days of Trump’s presidency, largely due to expectations that the new administration would focus on deregulation and other pro-business initiatives. Instead, tariffs emerged as the major policy goal. That shift has created significant uncertainty about the prospects for inflation, employment, consumer spending, and other major drivers of economic growth—which, in turn, has weighed heavily on stock prices.

Despite the S&P 500’s near-historic nosedive under Trump thus far, other areas of the equity universe remain strong. For example, international stocks, as measured by the MSCI ACWI ex USA Index, are up 7.9% since January 20. Even among U.S. stocks, sectors such as utilities and consumer staples are outpacing the broader market.

The upshot: We believe well-diversified portfolios can help investors weather recent U.S. underperformance and stay on track toward their key goals-based investment objectives.