The poverty rate for widowed women in the U.S.

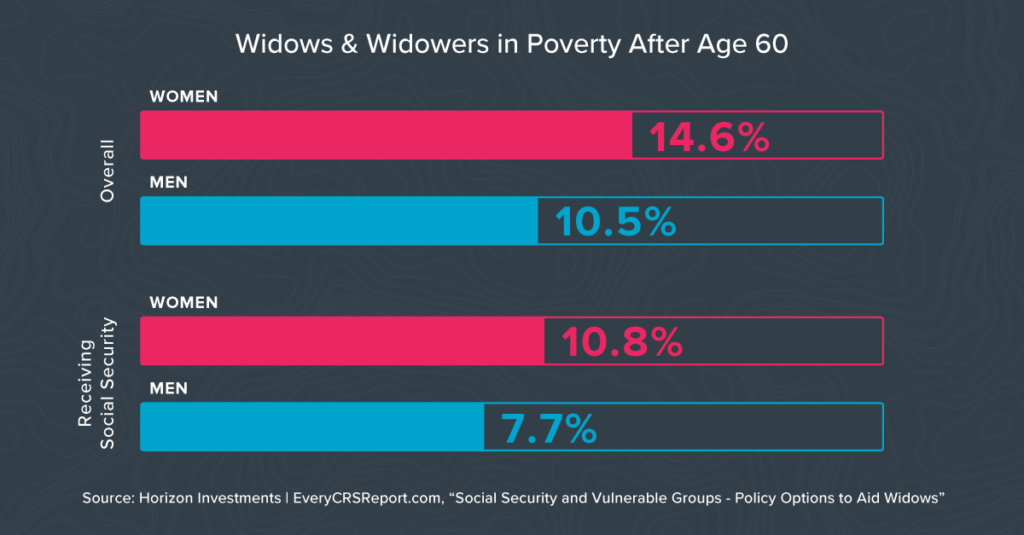

Of all the financial challenges facing retirees, being a widow can be one of the most difficult to bear. As the U.S. comes to the end of National Women’s History Month, Horizon Investments is exploring the potential financial risks widows face. As of 2017 (the most recent available data), 14.6% of widows aged 60 and above were living in poverty. That’s an improvement over years past, yet it shows there’s a need for individualized financial planning. And a goals-based approach – because it focuses on personalized results – can be well-suited to the task of protecting a widow from financial strain.

As millions of two-income, Baby Boomer households begin retirement in the decade to come, their financial wealth heading into this new stage of life doesn’t necessarily insulate them from the possibility of a large reduction in income after the death of a spouse. The monthly Social Security benefit cut for widows ranges from 33% to 50%, compared to the couple’s combined benefit1. The situation can be made worse if the deceased spouse’s pension plan benefit is reduced or eliminated, making it all the more important to have a nest egg or another financial safety net to bolster household wealth. In that situation, goals-based planning can help greatly by identifying key risks to achieving the goal of a secure retirement and offering specific solutions.

Can you live on $22,000 a year?

For some women, their annual retirement income may be shockingly small. Among widows aged 65 and older, about 51% live on less than $22,000 a year, according to WiserWomen.org2.

A widow’s financial wellbeing is also made more vulnerable by life longevity and health issue risks. Women are estimated to live three to five years longer than men, and women are at higher risk of developing Alzheimer’s4, which may cause higher health care costs later in life.

It’s estimated that 51% of women enter a nursing home after age 70 versus 38% of men3. In dollars and cents, the longest-lived women have out-of-pocket nursing home expenses of $75,310, 44% larger than the $52,365 for men4.

Some good news

The hopeful news is that as increased numbers of women spend more time in the workforce, they may increase their lifetime savings and Social Security benefits. A study by the Center for Retirement Research at Boston College found that the average number of years widows were in the workforce climbed to 25 years in 2014, up from 15 years in 1994. The group predicted it would rise to 32 years by 20295. However, some 30% of women are not saving for retirement, according to a survey last summer by the Transamerica Center for Retirement Studies6. That’s a far larger proportion than men who aren’t saving at 19%.

Difficult conversations that are worth having

Even with improving financial awareness and more savings, Social Security system researchers are advocating for changes to the program to reduce the risk of poverty for widows1. Financial advisors should be prepared to bring up a topic that, admittedly, is difficult to talk about. Making it more of a challenge is that women have historically admitted to being more reluctant than men to discuss retirement. Of those surveyed by Transamerica, 22% of women, versus 18% of men, responded that they never discuss retirement with family and close friends.

Retirement issues are becoming more complex and more personal as the responsibility of saving and investing is shifting to workers from employers. We believe the importance of robust, individualized, goals-based planning will only increase in the years ahead as more women build their nest eggs at various companies and have to consider how to navigate the challenges of living longer. And that’s especially true of Baby Boomers, many of whom may carry with them a mix of pensions, 401-Ks, IRAs and investments. Researchers estimate that 2020 marked the halfway point in the wave of Boomer retirements. It will take until 2030 for everyone in that generation to be at least 65 years old7.

1 EveryCRSReport.com, “Social Security and Vulnerable Groups – Policy Options to Aid Widows,” January16, 2020

2 WiserWomen.org, “Widowhood: Why Women Need to Talk About This Issue”, 2019

3 EBRI.org, “Cumulative Out of Pocket Health Care Expenses After the Age of 70”, April 3, 2018

4 WiserWomen.org, “Women’s History Month: A Time to Reflect on Women’s Retirement Challenges”, 2018

5 FA-MAG.com “Widows Are Becoming Less Likely to Fall Into Poverty, Study Finds”, July 3, 2018

6 Transamericacenter.org, “Women and Retirement: Risks and Realities Amid COVID-19 September 17, 2020

7 Census Bureau, “By 2030 All Baby Boomers Will Be Age 65 or Older”, December 2019

Further reading:

Essentially Nothing. That’s How Much Bonds May Return Over Next Five Years

It’s Getting Harder to Fund Retirement Using Bonds

If Inflation Returns, Bond’s Diversification Power May Disappear

Disappearing Junk Bond Yields

Soaring Innovation Companies Go Cold as Interest Rates Rise: Big Number

Inflation Could Be Coming, Are You Ready?

Small-Cap EPS Growth Expected to Be 4x Faster Than S&P 500

Biden, Trump Agree: Make America’s Growth Great Again

This commentary is written by Horizon Investments’ asset management team. For additional commentary and media interviews, please reach out to Chief Investment Officer Scott Ladner at 704-919-3602 or sladner@horizoninvestments.com.

To download a copy of this commentary, click the button below.

To discuss how we can empower you please contact us at 866.371.2399 ext. 202 or info@horizoninvestments.com.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments. Index information is intended to be indicative of broad market conditions. The performance of an unmanaged index is not indicative of the performance of any particular investment. It is not possible to invest directly in an index.

Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent.

Other disclosure information is available at hinubrand.wpengine.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2021 Horizon Investments LLC