One of the most confounding aspects of trying to anticipate whether inflation is getting better or worse is the constantly changing drivers of rising prices.

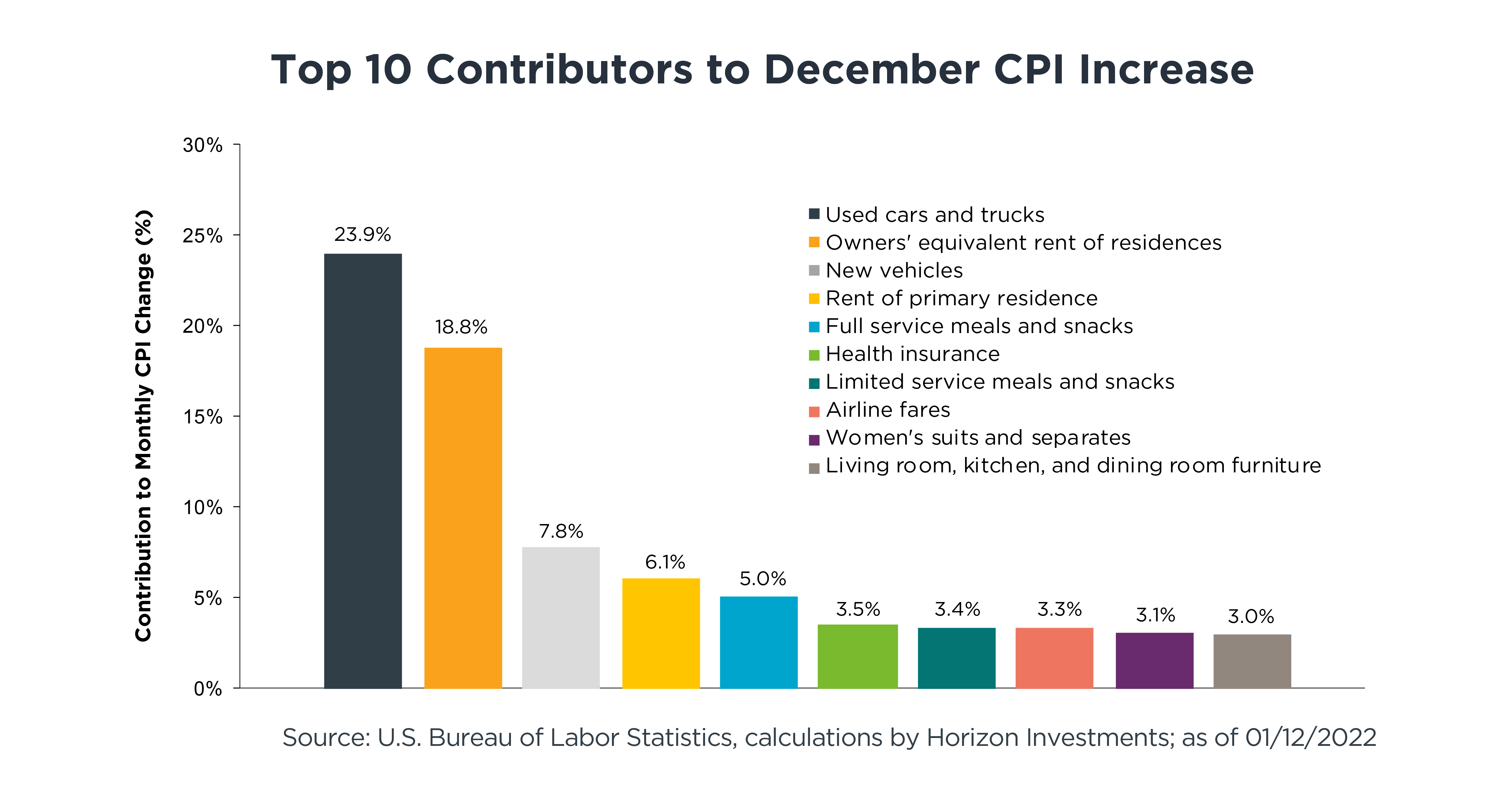

Used car and truck prices are back as the leading cause of inflation, accounting for nearly a quarter of the 7% year-on-year increase in the December Consumer Price Index (CPI).1 That’s a reversal from August and September when used vehicle prices were a restraint on CPI.

Used car and truck prices reflect the same supply/demand imbalances that affect many items.

With new vehicles in short supply – and their sticker prices rising – many car shoppers are turning to the pre-owned market. The problem is that the spillover demand is so strong that used-vehicle shoppers are having to pay up if they truly want that set of wheels.

The too-little supply, too-much demand mismatch – which we thought would ease by now – continues in other areas, from homes to appliances to lumber (yes, it’s price is rising dramatically again).2

The dramatic spike in omicron cases threatens to inflame the near-term inflation picture. Workers calling out sick could dent manufacturing output, slow the unloading of ships at ports, or impact the movement of goods to warehouses and stores – all of which could keep inflation elevated. However, if omicron passes quickly, the hiccups to supply chains may be short-lived, and the inflation threat probably will be minor. It’s a waiting game.

The kaleidoscope of moving parts that currently feed into inflation make it nearly impossible to forecast when a semblance of normalcy will return. Instead, we‘re focusing on the incoming data for clues about whether relief is in the pipeline. While the December CPI reading was shocking, last week’s Big Number looked at the dramatic improvement in a manufacturing inflation report and whether that indicated if we are near a peak in these painful consumer readings.

The key things we are monitoring on inflation in 2022 are: one, a shift in consumer spending from goods, like automobiles, to services, such as restaurants; two, improving supply chains; and, three, the economic impact of interest rate hikes. Higher rates, both here and abroad, could slow GDP growth, and that might mean we will see less inflation pressure.

One additional thing that’s on our radar, apartment rents and what’s called “owners’ equivalent rent of residences” – which attempts to estimate how much a homeowner would pay if they rented their home instead of owning it. It was the second biggest contributor to December’s CPI increase (see chart above). We will have more to say about that issue in our Q4 Focus, which is coming out soon.

We think goals-based investors, especially those who have a goal that’s far off in the future, may want to consider sticking to their saving and investing plan while talking with their advisor about whether any changes are necessary in light of the inflation news. In our view, staying the course can often be the hardest, but the best, thing to do.

Further Reading:

1 Bureau of Labor Statistics, www.bls.gov

2 Fortune, ‘’The Lumber Bubble Is Back,’’ Dec. 22, 2021

This commentary is written by Horizon Investments’ asset management team. For additional commentary and media interviews, contact Chief Investment Officer Scott Ladner at 704-919-3602 or sladner@horizoninvestments.com.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments. Index information is intended to be indicative of broad market conditions. The performance of an unmanaged index is not indicative of the performance of any particular investment. It is not possible to invest directly in an index.

Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent.

Other disclosure information is available at hinubrand.wpengine.com.

Horizon Investments, Risk Assist and the Horizon H are registered trademarks of Horizon Investments, LLC

©2022 Horizon Investments LLC