Comparing Historical IPO Waves to the Present

To understand what is different about today’s wave, it helps to examine prior waves. In the 1990s, public markets were the primary source of growth capital. Amazon went public in 1997 at a valuation of $438 million, with less than $16 million in annual revenue, just three years after its founding. Netscape was barely a year old at its IPO, valued at around $2 billion on its first day of trading. Google went public at a $23 billion valuation in 2004. Facebook, then the largest tech IPO on record, debuted at $104 billion in 2012 when it was eight years old. In the 1990s, hundreds of companies entered the public markets each year, giving investors a broad set of opportunities. Today’s IPO wave revolves around a handful of companies that are going public later, larger, and at higher valuations than their 1990s counterparts.

Exhibit 1: Number of IPOs by Year (1990-2025)

Jay Ritter, University of Florida, data as of 06/05/2026.

The difference isn’t that these are better businesses. Over the past two decades, private capital markets have expanded dramatically, providing growth funding that once came primarily from public investors. Venture capital, private equity, and sovereign wealth funds now deploy hundreds of billions of dollars, allowing companies to reach enormous scale before going public. By the time firms like SpaceX or OpenAI eventually list, much of their most explosive growth may already have accrued to private investors.

That is not necessarily a problem. Amazon, Google, and Facebook generated substantial gains both before and after their IPOs, creating enormous value for public shareholders. The key difference today is the starting point. Public investors are often entering later and at much higher valuations, making disciplined analysis more important than ever.

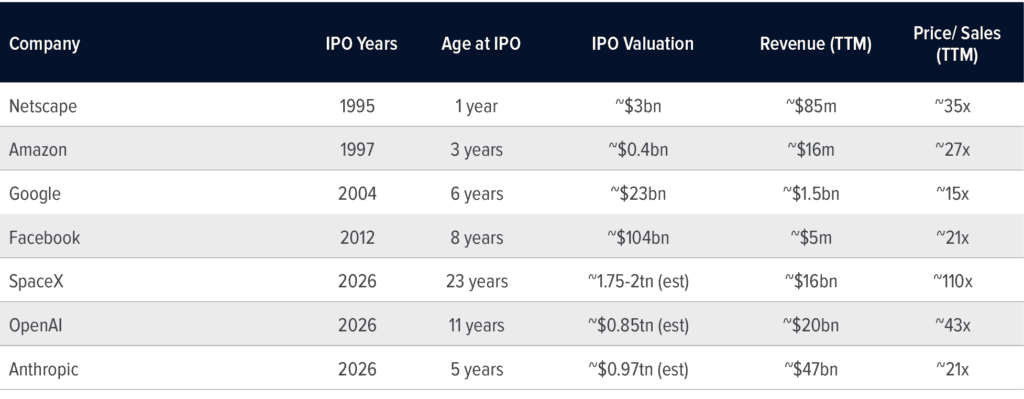

Exhibit 2 illustrates this well. Anthropic’s estimated price-to-sales multiple of around 21x is comparable to Facebook’s at its 2012 IPO and considerably more grounded than SpaceX’s 110x or OpenAI’s 43x. These are not the same investment proposition and should not be evaluated as such.

Exhibit 2: Then vs. Now – IPO Valuations at a Glance

SEC EDGAR (historical prospectuses); SpaceX S-1 filing; press reports (OpenAI, Anthropic), 06/05/2026, TTM: Trailing Twelve Months

Historical IPO Performance and Volatility

The historical record on IPO performance reinforces the need for caution: the valuation at entry and timing can be as important as company quality. The average IPO underperforms the broader market over a three to five-year time horizon. According to research by Jay Ritter of the University of Florida, who has tracked IPO performance since 1991, the initial run-up accrues almost entirely to institutional holders. The 2020-2021 IPO cohort illustrates this clearly. Retail investors, flush with COVID-era stimulus, bid them up. After this initial demand, sustained underperformance followed as rates rose and growth multiples compressed. We are currently in a similarly hot macro environment, with risks of higher rates.

The biggest risk is not that these companies fail to create value over the long run. The journey to that value can be long, volatile, and unforgiving for investors who buy at the wrong price or sell at the wrong time. For example, investors who bought Amazon at its IPO in 1997 and held their shares through the dot-com collapse and the company’s eventual recovery earned significant rewards a decade later. However, the path was not linear, and timing mattered at every point along it. Investors who bought near the 1999 peak watched their gains evaporate, falling more than 90% from that high and facing years of losses before the stock recovered. Investors who bought at the IPO, rode the wave to the peak, and sold on the way down locked in losses on a company that went on to become one of the greatest wealth creators in market history. The experience of investors who bought at the wrong moment, or sold at the wrong moment, was a different story entirely.

The lesson is not to avoid these companies. It is to understand that volatility creates a specific and underappreciated risk: the combination of a strong initial run-up, the eventual evaporation of early gains, and the behavioral pressure to sell at precisely the wrong moment. Patience and entry point matter as much as conviction in the underlying business.

Exhibit 3: Amazon Stock Price, 1997-2007