U.S. stocks posted strong returns during the second quarter of 2025, but the path to those gains was anything but smooth. In early April, stocks had plummeted nearly 20% from their highs due to President Trump’s plan to impose sizable and widespread tariffs on imports, fueling fears of higher inflation and a recession.

Trump repeatedly backed down from the most extreme of his trade policy threats throughout the quarter, however, revealing that the man-made, self-inflicted challenges created by the tariffs could also be rapidly un-man-made. Tariff reversals gave investors the confidence to push stock prices higher. In stark contrast to the losses seen during the first quarter of 2025 (see Exhibit 1), major U.S. indices all finished in the black during the second quarter—with both the S&P 500 and the Nasdaq 100 ending the quarter at record highs. Tech stocks posted some of the biggest gains, while small-cap stocks continued to lag their larger peers.

For the quarter:

- The Nasdaq 100 index was up 17.9%.

- The S&P 500 index gained 10.9%.

- The S&P 600 index of small-company stocks rose 4.9%.

International stocks also delivered strong results, with less volatility than U.S. equities. The MSCI ACWI ex-U.S. index of developed and emerging international markets—which covers approximately 85% of the global equity opportunity set outside of the U.S.—was up 12% during the quarter, building on its first-quarter outperformance versus domestic indices (see Exhibit 1). Despite the potential impact of a trade war, many investors favored the relative stability offered by foreign companies and governments.

EXHIBIT 1: MAJOR STOCK MARKET INDICES RETURNS 2Q 2025

Bloomberg, calculations by Horizon, data as of 07/09/2025. Past performance is not indicative of future results. It is not possible to invest directly in an index.

Bloomberg, calculations by Horizon, data as of 07/09/2025. Past performance is not indicative of future results. It is not possible to invest directly in an index.

Bond yields ended the quarter close to where they began, with the yield on the 10-year U.S. Treasury roughly flat from three months earlier. That said, yields rose sharply at various points throughout the quarter, driven by concerns that U.S. fiscal and trade policies were making government debt riskier. Unsurprisingly to many investors, credit rating agency Moody’s downgraded the U.S. credit rating during the quarter, citing the nation’s inability to address large and growing deficits. In that uncertain environment, the yield curve steepened as investors demanded increasingly higher yields in exchange for holding longer-term government securities. Meanwhile, the Federal Reserve Board has maintained a key short-term interest rate steady throughout the quarter, waiting to see how the economy responds to tariffs before deciding whether to raise or lower rates.

ALL THE FEELS

Despite the positive returns among stock markets, confusion over government policy decisions during the quarter left consumers, business leaders, and investors feeling nervous, even downright pessimistic:

- Far more consumers expect their financial situation to be worse a year from today compared to those who expect it to be better (see Exhibit 2).

- More consumers anticipate having lower incomes in the future than those who expect higher incomes, according to the University of Michigan.

EXHIBIT 2: UNIVERSITY OF MICHIGAN (UMICH) EXPECTED CHANGE IN PERSONAL FINANCIAL SITUATION BETTER MINUS WORSE

Bloomberg, calculations by Horizon, data as of 06/30/2025.

Meanwhile, among businesses, uncertainty is the prevailing watchword—literally: A recent Fed Beige Book (compiled from interviews conducted with the business community) mentions the word “uncertainty” 80 times, up from just 10 mentions a year ago.

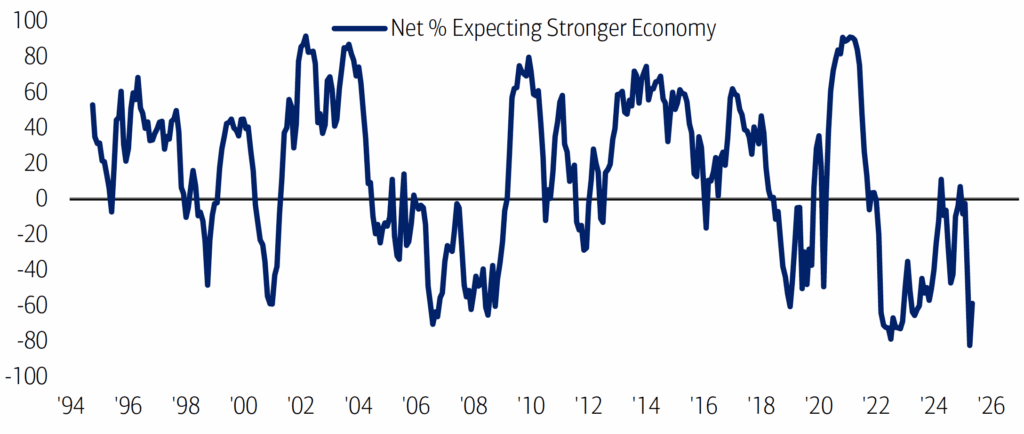

Even many investors aren’t particularly upbeat these days. In the second quarter, professional fund manager sentiment dropped to its fifth-lowest level since records began in 2001. That drop was mainly because the vast majority of investors foresee weaker economic conditions over the next 12 months (see Exhibit 3).

EXHIBIT 3: NET PERCENTAGE OF FUND MANAGERS WHO SEE A STRONGER GLOBAL ECONOMY OVER THE NEXT 12 MONTHS

FMS: Fund Manager Survey. Bank of America, data as of 05/13/2025

ALL THE REALS

Neither Wall Street nor Main Street is brimming with hope for the future. However, that sour mood doesn’t accurately reflect an important fact: Many key economic indicators have thus far remained strong and resilient in the face of recent uncertainty. For example:

1. Economic growth: After fluctuating wildly during and after the pandemic, nominal U.S. Gross Domestic Product (GDP) has returned to its typical growth rate of approximately 5% (see Exhibit 4).

EXHIBIT 4: U.S. GDP

Bloomberg, calculations by Horizon, data as of 05/28/2025.

2. Corporate revenues: Similarly, sales growth among U.S. corporations is on par with the growth rates seen during most nonrecessionary periods over the last 25 years, according to St. Louis Federal Reserve Data.

3. Employment: Given that the current GDP and revenue growth rates are within the normal range, it follows that unemployment has remained low. While businesses overall are now hiring new workers at a slower rate than they have been in recent years, they are generally not laying off or firing their existing staff (see Exhibit 5). Simply put, most people who want jobs are both employed and are staying employed—giving them the continued ability to spend and save. Likewise, total payrolls are growing at a strong enough rate to support continued healthy consumer spending.

EXHIBIT 5: HIRING RATE AND LAYOFF RATE

Bloomberg, calculations by Horizon, data as of 05/28/2025.

Bloomberg, calculations by Horizon, data as of 05/28/2025.

The upshot: Much like the “vibe-cession” of 2023, people’s negative feelings these days are largely out of sync with the generally positive economic reality we find ourselves in.

THE AI OPPORTUNITY EXPANDS

One likely factor supporting the economy’s continued resilience is the growing role of artificial intelligence (AI). AI’s ability to fuel greater productivity and efficiencies has been well established, and businesses have responded by investing heavily in the technology in ways that are already generating positive outcomes.

Looking beyond the current disconnect between perception and reality, we see that AI remains perhaps the most powerful force in shaping the future global economy, and therefore will likely be a key driver of investment returns:

- AI today is the Internet of the mid-1990s: AI offers the same powerful transformative potential that the Internet did when it first gained momentum in the mid-1990s. It is easy to use and navigate, with obvious and immediate benefits. It can be applied in multiple ways across virtually all industries and sectors of the economy. It increasingly demonstrates the ability to enable users to enhance their productivity meaningfully.

- Agentic AI will be a game changer: The next stage of AI is agentic AI, which is designed to make autonomous decisions to solve users’ complex, multi-step requests and challenges. Agentic AI is poised to drive substantial productivity gains and operational efficiencies across industries, with potential significant impacts on companies’ top-line and bottom-line growth rates.

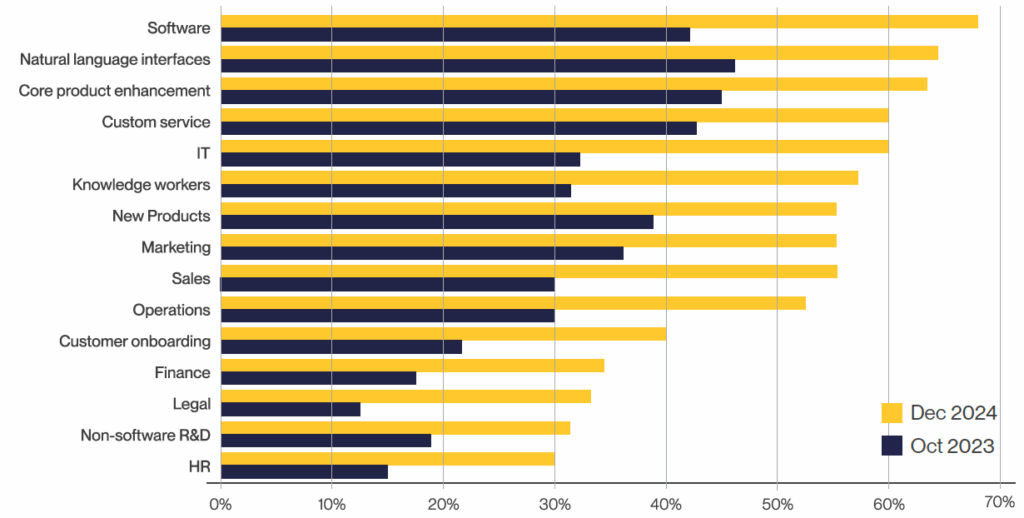

- AI adoption rates are rising fast: AI’s potential is already being realized, as it has rapidly become a core component of corporate strategy. In less than a year, for example, the growth of AI adoption in key business functions, such as information technology, core product enhancement, customer service, and marketing, has been immense (see Exhibit 6).

EXHIBIT 6: GENERATIVE AI ADOPTION, OCTOBER 2023 VS. DECEMBER 2024