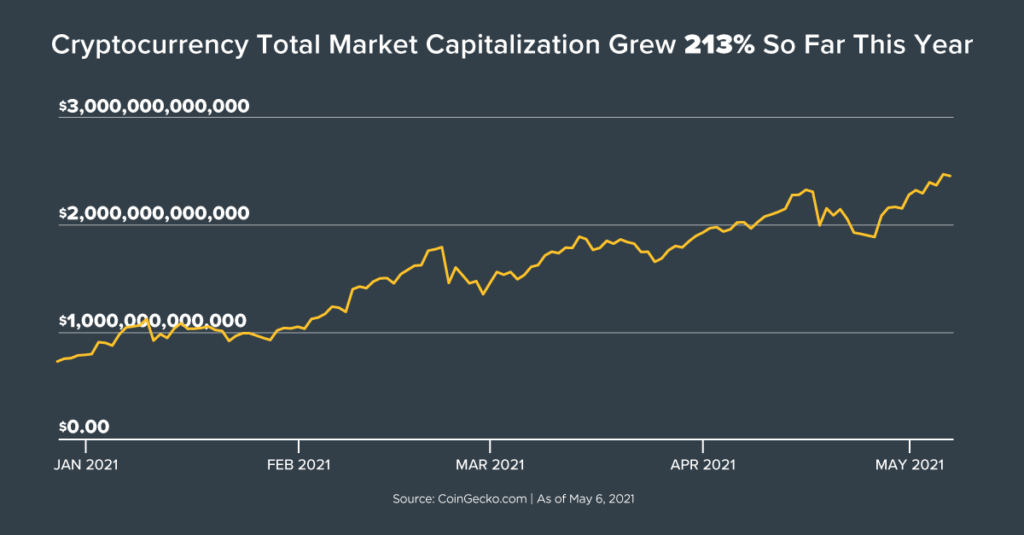

Total market capitalization of cryptocurrency has tripled so far this year to $2.46 trillion, according to CoinGecko.com

What was a rumbling of change in the last few years is now barreling into the mainstream with widespread name recognition of Bitcoin and the blockchain technology on which it’s built.

With fame has come fortune for some early cryptocurrency adopters, leading to an investment surge in coins and the companies involved in crypto. At times it’s felt like a frenzy this year as retail investors try their hand at trading crypto. A growing number of trading platforms, such as Coinbase and Venmo, are helping to drive the public’s interest.

The booming crypto industry is producing a zoo of new coins daily with Bitcoin being merely the best known. There are some 7,139 coins in existence, according to CoinGecko.com as of May 6.

Some people are convinced cryptocurrencies – and the computer networks they represent – mark another digital transformation of the economy and will displace our current banking and payment systems. That belief, along with a strong dollop of investor speculation, is helping propel the market capitalization of all cryptography-derived coins to $2.46 trillion from $787.1 billion at the end of 2020, according to CoinGecko.com.

Is it worthwhile to add cryptocurrencies to a goals-based investment plan? Will the investment frenzy die down or get more intense? Here are the questions financial advisors’ clients may be asking and Horizon Investments’ view of this current trend within a goals-based investment framework.

Is Bitcoin a currency and will it be used to conduct business?

For Bitcoin (or any asset, from gold to tokens) to become a currency it has to fulfill three essential functions:

➤ A store of value ➤ A means of exchange ➤ A unit of account

At present, Bitcoin does not fulfill any of those roles, though that doesn’t prevent it or another coin from fulfilling those purposes in the future.

To be a store of value, the key attribute is price stability over long periods of time. Bitcoin’s wild price swings in its brief existence have made it a media darling, but that’s not necessarily going to give someone comfort that their savings denominated in that asset are safe and secure. Bitcoin is sometimes called “digital gold” as some argue it can displace the precious metal as a store of value. The difference, however, is that gold has been prized for thousands of years as a precious item, is a tangible thing and can be physically held and people the world over still want to own it. While both gold and Bitcoin prices rest mainly on how much someone is willing to pay for them, Bitcoin has two disadvantages and one advantage. The downside is that buyer interest might change if a better digital payment technology comes along. And there remains the possibility that future government regulations limit or outlaw Bitcoin’s use. One helpful characteristic of Bitcoin is that it is generally easier to transport within an electronic wallet on a USB drive than gold coins and bars – assuming, of course, that someone has the internet access that’s required to use the cryptocurrency.

As a means of exchange, Bitcoin would have to be universally accepted as payment for goods and services. Bitcoin currently is not legal tender and no merchant or business has to accept it. Companies that are letting buyers use the cryptocurrency, such as Tesla did until this week, are doing so voluntarily. Fiat currencies, in contrast, are issued by countries as legal tender to pay taxes and make purchases, are backed by the full faith and credit of that country and are trusted by people as a means of exchange due to the integrity of a country’s political and economic systems.

As for a unit of account, note that companies allowing buyers to use cryptocurrency are not pricing their goods in terms of Bitcoin. For example, Tesla priced its cars in dollars and then converted that to a Bitcoin price; it was not pricing its cars in Bitcoin (see Tesla’s FAQs). This distinction is critical. If Tesla decided to price its cars in terms of Bitcoin, there would be no need for a U.S. dollar price. You could exchange, say, two Bitcoins for a Tesla Model X – irrespective of how many U.S. dollars those two Bitcoins represent. That is distinctly NOT what Tesla did – it priced the cars in U.S. dollars and accepted an equivalent number of Bitcoins, based on the U.S. dollar value at the time of the transaction. Bitcoin, then, is not currently fulfilling a currency-defining role as a “unit of account.”

Lastly, there’s the rising Bitcoin network congestion which is driving up the fee per transaction. On April 21, the average fee was $62.78, according to bitinfocharts.com, making the cryptocurrency all but unusable for small, everyday purchases.

Is Bitcoin, and crypto generally, still a speculative investment?

Yes. Despite the growing embrace of Bitcoin by established U.S. companies and widespread trading interest, it’s Horizon Investments’ view that the crypto space remains a speculative and highly volatile investment. Bitcoin prices move mainly on supply and demand and sentiment, leaving investors with little sense of whether it has intrinsic value.

Contrast the problem of valuing Bitcoin vs. valuing a U.S. Treasury security. There is a general consensus in the financial community on the pricing model for a Treasury security is and what inputs go into that model: the dates of future cash flows and the amounts of those cash flows. Using that information, the market comes to a general consensus on the price of a Treasury – though people may differ on whether they think interest rates will rise or fall in the future, and that debate makes a market. In the case of Bitcoin, what should be the inputs into its price? The number of coins in existence, the computing power needed to mine an additional coin, some measure of the value of a dollar, some measure of supply and demand? Without general agreement, there is uncertainty about Bitcoin’s fundamental value – this, in our view, is one of the primary drivers of the volatility that cryptocurrencies have experienced since their inception. Additionally – and just as importantly in our view – you cannot impart a valuation to Bitcoin without knowing what future government regulations will be for cryptocurrencies.

Bitcoin may not be a currency but it has been on a spectacular run. Does it, and crypto generally, fit into a goals-based plan?

The financial planning industry is moving towards goals-based financial plans and portfolios, which are constructed to maximize the probability that a client’s financial plan will be realized under various possible scenarios. The goals-based issue with cryptocurrencies is that their short life span (Bitcoin was only invented in 2009) means not enough is known to make any definitive conclusions about either long-term returns or how to integrate them when constructing a portfolio.

There has been some research that shows Bitcoin may be uncorrelated with the other major asset classes: stocks, bonds, currencies, commodities. However, it’s too soon to know how portfolio diversification is helped by owning Bitcoin specifically or crypto in general. In addition, crypto’s volatile price movements make it difficult for advisors to deliver on what we call “expectational certainty” in goals-based plans under various macro-economic conditions: understanding how an asset is likely to behave (either based on theory or based on historical observations) in different economic and market conditions is crucial when constructing goals-based portfolios.

We believe advisors should ask clients how Bitcoin/cryptocurrencies would fit into their goals-based plan and why they’re interested in owning them. Risk taking can be part of a financial plan, but it may be a good idea to remind clients that a disciplined plan of action is needed if they are going to avoid the investor behavior pitfalls that can affect returns.

Does Horizon currently invest in cryptocurrencies?

Horizon Investments does not currently own cryptocurrencies in its portfolios, though it is possible that we may at some point in the relatively distant future. One of the reasons for that is without clarity on either long-term performance or the future regulatory framework for cryptocurrencies, it may be challenging to find a place for an asset like Bitcoin in a goals-based portfolio.

To be sure, there is nothing wrong with speculative investments, per se – but we believe it is impossible today to assess the risks and rewards of an investment in something like Bitcoin. Without the ability to make that assessment, we cannot put our client’s money at risk – even if we end up being wrong in hindsight.

Can governments regulate crypto out of existence?

Perhaps. Crypto enthusiasts and innovators say it’s impossible to eradicate as no one person or group controls the decentralized computer systems and open source computer code that are the foundation of the crypto industry. That said, it seems unlikely that any sovereign nation would allow their currency – which is a source of power – to be replaced by a cryptocurrency that they have no control over and that gives its users anonymity. For many governments, anonymity is a bug not a feature of crypto. And it’s our opinion that governments, including the U.S., will likely write future regulations that force the crypto industry to adopt know-your-customer rules, anti-money laundering laws and other anti-crime statutes. We believe it is simply not in a sovereign nation’s best interest to allow cryptocurrencies to “take over” the financial system in their country.

We should add here that central banks are working on a digital version of fiat currency, a development which may curtail Bitcoin’s use as a means of exchange. Dubbed central bank digital currency (CBDC), the digital dollars or euros or yen would likely be legal tender for transactions, with fund transfers presumably recorded using blockchain technology. It should be noted that CBDC are NOT cryptocurrencies – CBDC are fiat money, just in digital form. As such, the government could require merchants to accept it – something that is not currently being required with cryptocurrencies.

If after talking through the points above clients want to own Bitcoin or other coins as part of a larger portfolio, what framework should they use to think about an appropriate amount of risk taking?

While Horizon doesn’t endorse investing in Bitcoin or other cryptos, in our view, any investor willing to risk their capital in cryptos might want to first consider the uncertainties and speculative trading aspects involved. However, it should be noted that Bitcoin has exhibited at times a positive correlation to the equity market, for example the Russell 3000, so an allocation would not have historically been a diversifying investment from a portfolio construction standpoint.

Horizon’s bottom line is that crypto investing is not yet ready for mass adoption in goals-based financial plans. Its brief history, volatile price and the potential for future regulations – among many other issues – make it difficult to assess if crypto can be helpful in meeting a client’s financial objectives. We are monitoring for conditions that we believe would make cryptocurrency a potentially attractive investment in a goals-based portfolio; however, at the time of this writing, we do not see those conditions as close to being met.

To download a copy of this commentary, click the button below.

Further reading:

Capital Gains Taxes and the S&P 500: Complete Strangers for Over 60 Years

Inflation Fixation, Bubble Trouble and Goals-Based Planning: Market Notes

Americans Retiring Early May Benefit from a Goals-Based Solution

Widows Are at Higher Risk of Falling Into Poverty

Many Investors Tried to Trade the Pandemic Plunge in Stocks

Are Bonds in a Bear Market? That’s the Wrong Question to Ask

If Inflation Returns, Bond’s Diversification Power May Disappear

Essentially Nothing. That’s How Much Bonds May Return Over Next Five Years

High & Mighty Stocks; Feeling Inflationary?; Game Stopped: Market Notes

It’s Getting Harder to Fund Retirement Using Bonds

The Stock Market Is Strange, But Not Broken by GameStop: Market Notes

This commentary is written by Horizon Investments’ asset management team. For additional commentary and media interviews, please reach out to Chief Investment Officer Scott Ladner at 704-919-3602 or sladner@horizoninvestments.com.

To discuss how we can empower you please contact us at 866.371.2399 ext. 202 or info@horizoninvestments.com.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments. Index information is intended to be indicative of broad market conditions. The performance of an unmanaged index is not indicative of the performance of any particular investment. It is not possible to invest directly in an index.

Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent.

The Real Spend® retirement income strategy is NOT A GUARANTEE against market loss and there is no guarantee that the Real Spend® strategy chosen by an investor will be successful for the entirety of an investor’s retirement. Clients may lose money. Real Spend® is an asset allocation strategy that uses an investment model to (i) plan savings amounts and overall asset allocation during the distribution phase of retirement planning, (ii) compute target retirement wealth, assuming a retirement budget and a spending-investment strategy after retirement, (iii) compute the transition from the accumulation phase to the retirement phase, and (iv) generate the spending-investment strategy after retirement. Our retirement spending investment strategy uses an allocation model that replenishes cash needed for withdrawals. Before investing, consider the investment objectives, risks, charges, and expenses of the strategy. All investing involves risk. This strategy is not an insurance product with payments guaranteed. It is a strategy that invests in marketable securities, any of which may fluctuate in value. There is a possibility of outliving the assets if market performance is lower than forecasts used in planning, or if longevity is longer than anticipated. Investors should note that historical data suggests that higher Spend Rates will have a lower likelihood of success for the entirety of the retirement period than a lower Spend Rate would. Past performance and market data are no guarantee of future results and investor experiences will vary.

Other disclosure information is available at www.horizoninvestments.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2021 Horizon Investments LLC