Market participants have fled dollar-based assets, leading to dollar weakness

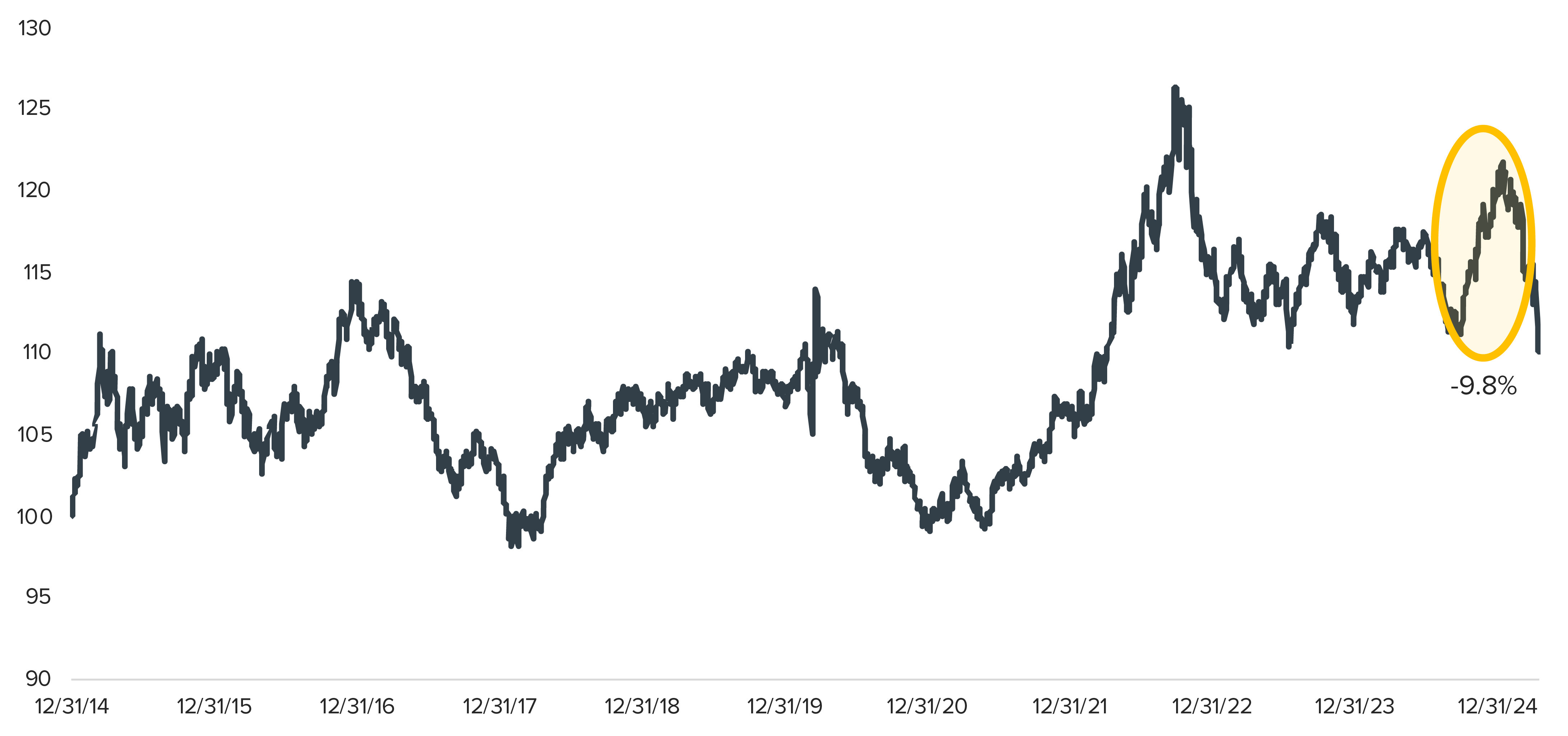

The U.S. dollar has experienced a sharp decline this year through April 17, falling 9.8% from its peak on January 13 and now sitting 4% lower than it was at the close of Election Day.

Year-to-date, this marks the worst start for the U.S. Dollar Index since 1990. While large drawdowns are not uncommon—the average annual decline since 1990 is -9.1%—it is rare for a move of this magnitude to occur so quickly.

In recent history, 2020 drawdowns followed massive Fed rate cuts during the COVID pandemic, and again in 2017 during the first year of President Trump’s previous term. However, in both cases, those drawdowns unfolded over nearly the entire year. By contrast, the U.S. dollar surged over 27% during the rapid interest rate hikes from 2021 through 2022.

The ICE U.S. Dollar Index

Source: Bloomberg, calculations by Horizon Investments, data as of 04/17/25.

Given recent tariff developments and the resulting extreme uncertainty, investors have exited dollar-based assets, as we previously noted. We believe the following market movements reflect this trend, and we will continue to monitor these correlations closely:

- U.S. equities have significantly lagged their International counterparts year-to-date, particularly within the technology sector.

- Long-term Treasury yields have surged following Liberation Day.

- Gold has extended its historic rally, rising over 25% year-to-date.

The premium valuations traditionally associated with U.S. equities have proven fragile, and we expect this vulnerability to persist amid continued uncertainty.

The upshot: Diversification remains essential—an important reminder amid the current weakness in dollar-based assets and the relative strength of international equities so far in 2025.