THREE POSSIBLE PATHS FORWARD

Scenario #1: Muddle Through

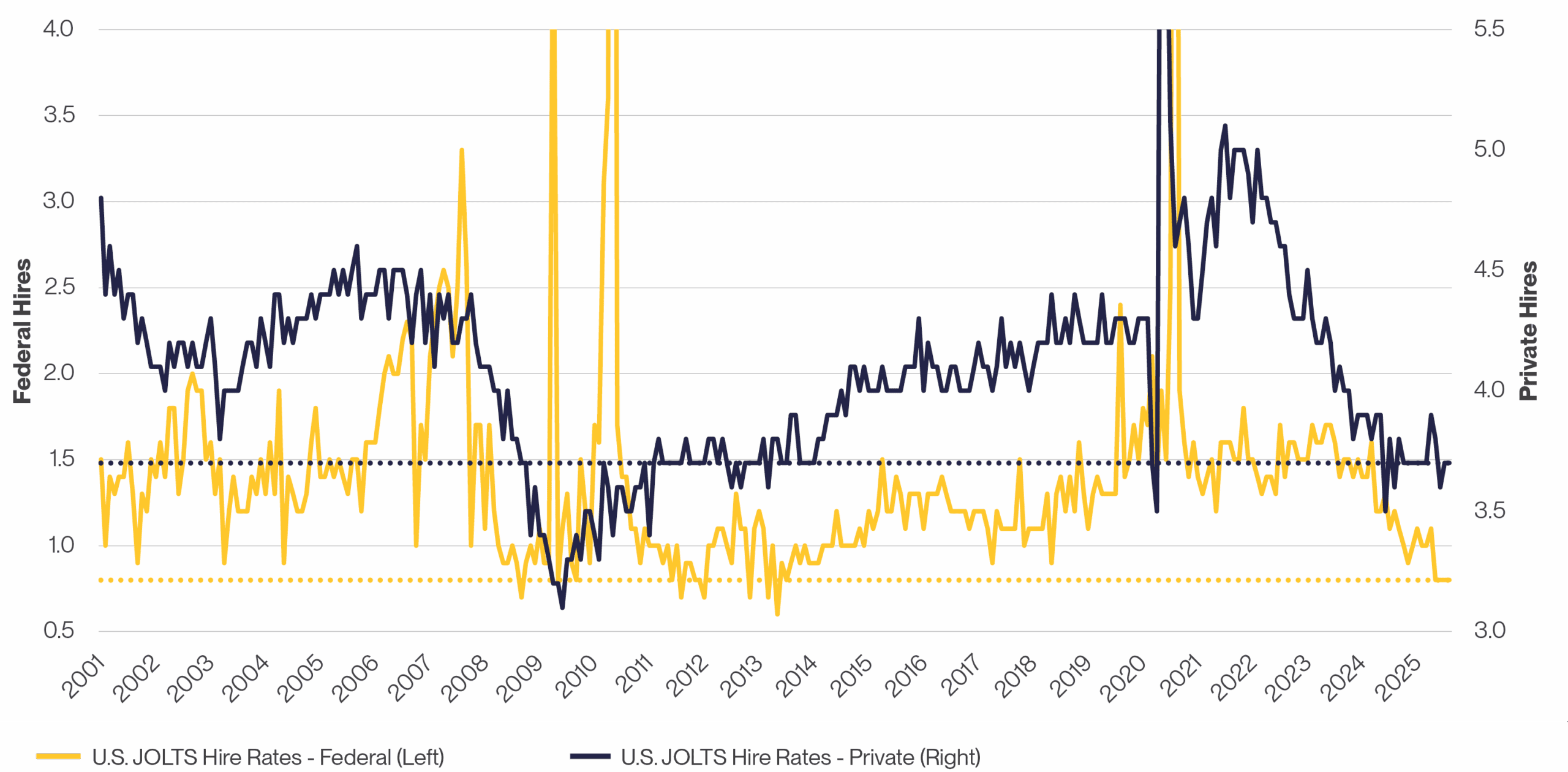

In a muddle-through scenario, we’d anticipate a continuation of mixed data signals, particularly focused on a cooling labor market and a strong U.S. consumer. For example, hiring momentum has slowed – as we saw in August, the economy added only 22,000 new jobs, falling short of the anticipated 76,500. The hiring rate among private companies is also hovering near historically low levels (see Exhibit 1).

EXHIBIT 1: U.S. FEDERAL AND PRIVATE HIRES RATES

Job Opening and Labor Turnover Summary (JOLTS)

Bloomberg, calculations by Horizon, 08/29/2025

However, those numbers overlook some important positives:

- Layoffs and firings are rare: The “low-hire” environment is being largely balanced by a “low-fire” mentality among businesses, as companies are hesitant to reduce the size of their existing workforces. The current rate of layoffs per 100 jobs in the private sector is just 1.2 — higher than it was a year ago, but still below pre-pandemic levels.

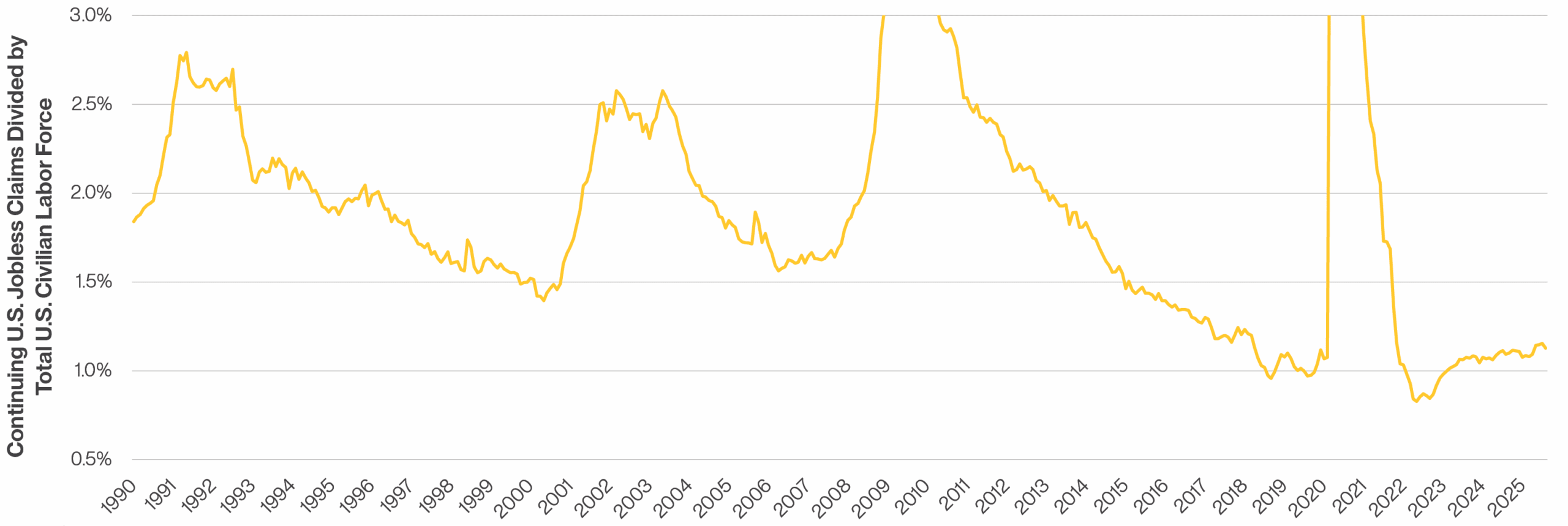

- Long-term unemployment is low: Although the labor market has somewhat weakened, it’s done so from a position of historic strength. Exhibit 2 shows that the share of the U.S. labor force experiencing ongoing unemployment remains near the record lows of 2022 and 2023.

EXHIBIT 2: PERCENT OF U.S. LABOR FORCE FACING CONTINUING UNEMPLOYMENT

Bloomberg, calculations by Horizon, 08/29/2025

Scenario #2: Growth Bust

That said, the labor market’s cracks could become full-on crevasses, leading us to a “growth bust” scenario. If the labor market suffers a major downturn or if fears of sudden unemployment start to accelerate, consumers, whose spending accounts for around two-thirds of U.S. economic activity, will likely tighten their purse strings. In that environment, an economic recession becomes a highly probable outcome.

Another area that investors need to closely monitor is corporate spending on artificial intelligence (AI) and other technologies. In recent quarters, technology spending has become a significant driver of gross domestic product (GDP) growth (see Exhibit 3). Companies are spending enormous sums on technology, particularly AI, and investors are rewarding those companies with higher valuations. Given how much this spending is helping support the overall economy, an unexpected reduction in tech capital expenditures could significantly weigh down growth.

EXHIBIT 3: U.S. REAL GDP GROWTH CONTRIBUTORS

J.P. Morgan, 09/02/2025

Scenario #3: Growth Boom

A third scenario involves growth accelerating from current levels, with both the economy and corporate profits strengthening. This outcome could result from factors such as:

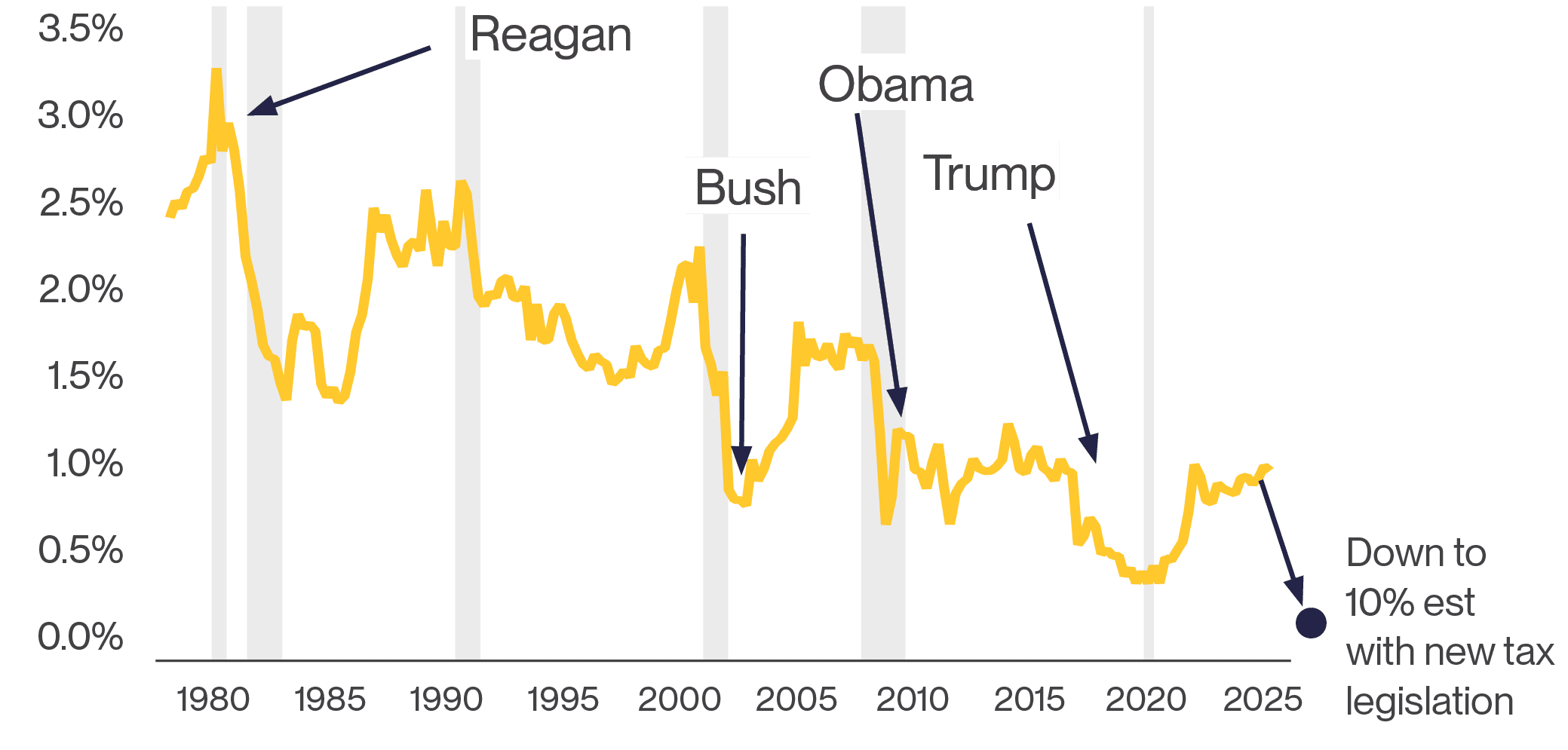

- Government policy: The domestic policy bill passed by Congress this summer is designed to push corporate tax rates down to historically low levels (see Exhibit 4), providing a boost to corporate profits going forward. Additionally, continued deregulation efforts by the Trump administration could benefit businesses’ top and bottom-line growth.

EXHIBIT 4: U.S. EFFECTIVE CORPORATE TAX RATE

Piper Sandler, 09/17/2025

Information obtained from third party sources is believed reliable but has not been vetted by the firm or its personnel.

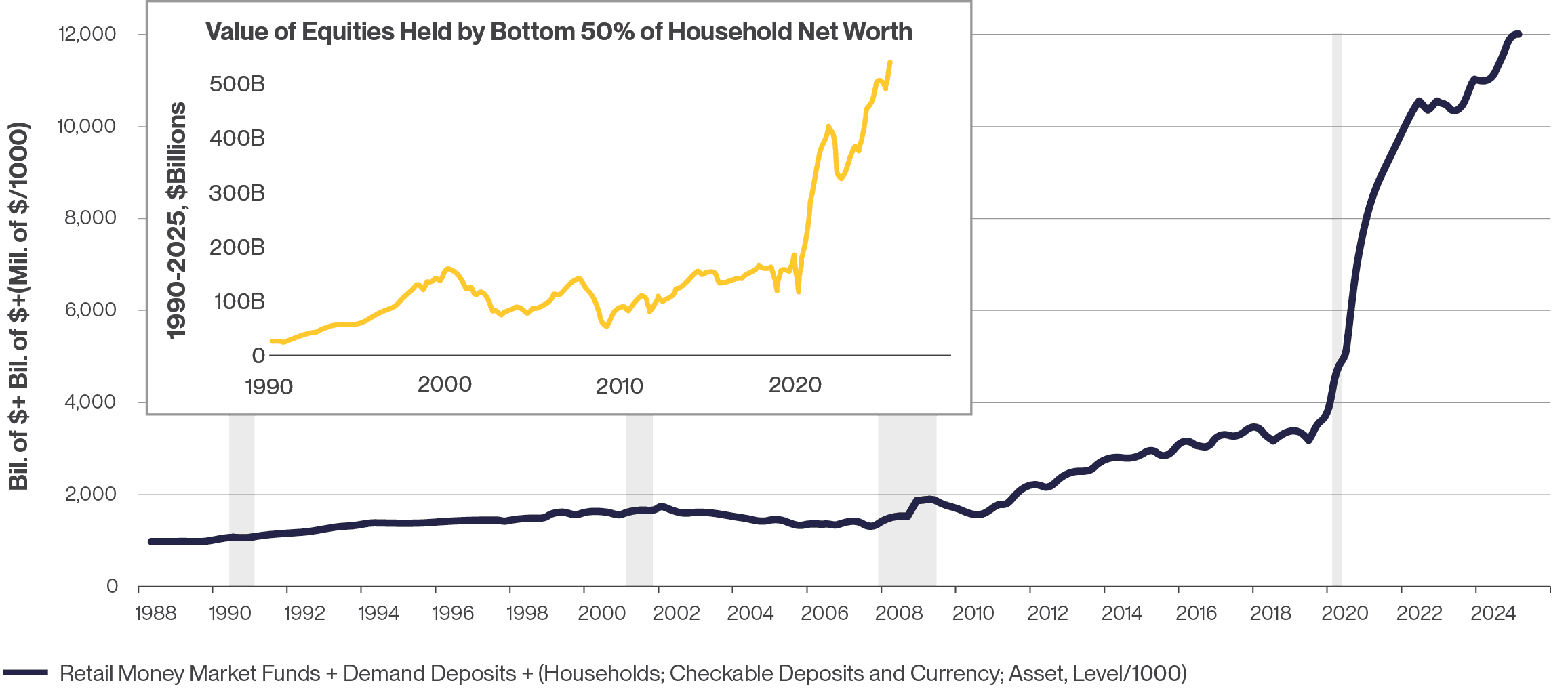

- Stronger consumer spending: Despite the falling consumer confidence noted above, the fact remains that consumers across wealth levels continue to be flush with liquidity and potential spending or investing power. Exhibit 5 shows that consumer assets held in money market funds and deposit accounts recently hit an all-time high, as did the value of equities held by households in the bottom 50% of net worth. Any number of developments, lower interest rates or greater trade policy clarity, for example, could prompt consumers to deploy that money into the economy, the financial markets, or both.

EXHIBIT 5: AMERICAN CONSUMER STILL FLUSH WITH LIQUIDITY

Shaded areas indicate U.S. recessions

Federal Reserve of St. Louis, 09/29/2025

Citadel Securities, 09/29/2025

Information obtained from third party sources is believed reliable but has not been vetted by the firm or its personnel.

CONCLUSION

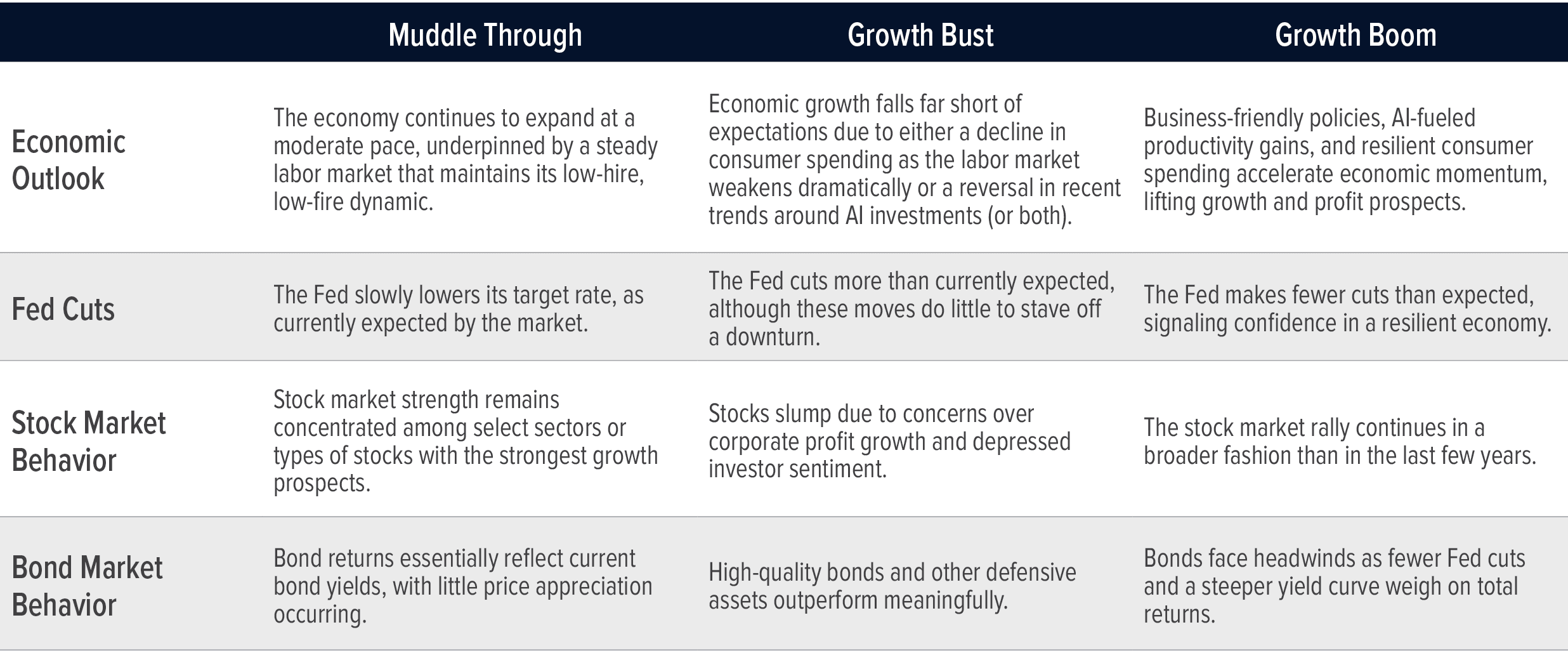

Each of these three scenarios comes with its own distinct implications for the economy, financial markets, and the Fed, which we’ve summarized below:

Over the next few months, our attention will remain focused on the labor market, consumer confidence, and spending patterns, as well as trends in the AI mega theme. Inflation readings and tariff impacts will affect both corporate profit expectations and adjustments to the Fed’s monetary stance.

No matter which of the three scenarios unfolds in the coming months, we will continue to apply both quantitative and qualitative insights to build resilient portfolios, designed to deliver thoughtful diversification amid uncertainty.