Put “protection” has come up short lately—but there’s a better way.

Put options are often a go-to risk management strategy among investors seeking protection against stock market declines. But for more than a year, puts have done little to safeguard many investors’ portfolios.

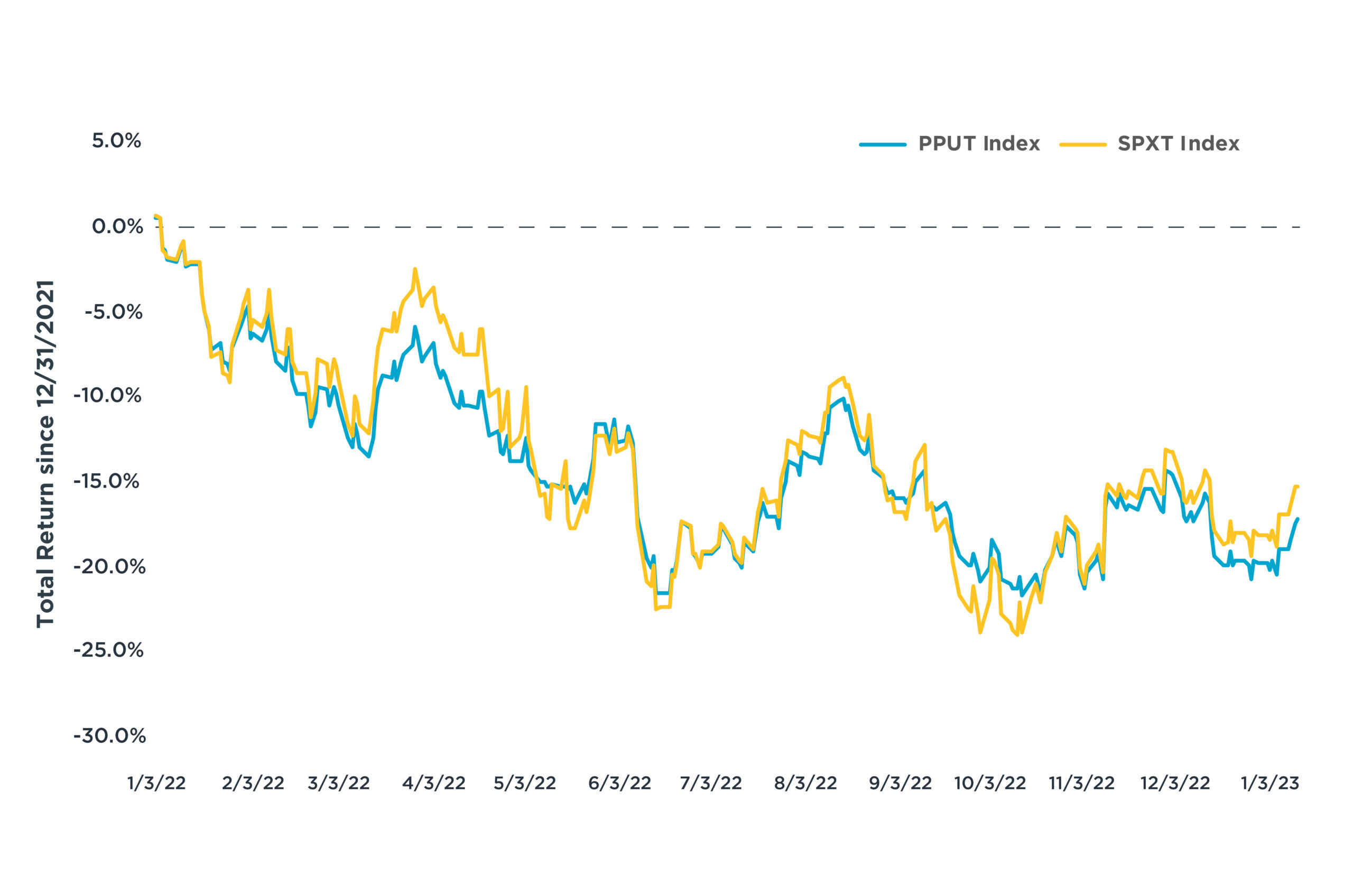

Case in point: While the S&P 500 Index is down 15.3% since the end of 2021, an index designed to protect investors from negative S&P 500 returns (the CBOE S&P 500 5% Put Protection Index, which tracks the value of the S&P 500 and a monthly 5% out-of-the-money put option) has fallen by 17.2%—1.9 percentage points worse (see the chart).

Ultimately, derivatives such as puts require investors to accurately forecast the market’s direction and timing of its movements. Puts have fizzled out largely because of the nature of the current equity market downturn. Stock prices’ surprisingly long and slow grind south, combined with elevated levels of volatility, have made put options more expensive—without the big and rapid market drops that cause puts to pay off. So, while put investors may have gotten the direction of stock prices right, they weren’t so lucky with the market’s drawn-out decline.

The good news: There are several ways to potentially mitigate this type of outcome while still taking advantage of the protection puts can offer investors. Some examples of active derivatives strategies include:

- Using an option collar, where call options are sold to reduce the price of the put options.

- Spreading out option maturities to minimize the risk of getting timing decisions wrong.

- Spreading out the strikes—the prices at which puts can be exercised— to reduce the risk of getting the magnitude of price movements wrong.

We believe having the flexibility to incorporate these types of active strategies can potentially generate more consistent, intuitive results—particularly when the markets don’t behave as investors (and their investments) want them to.

DISCLOSURE:

This commentary is written by Horizon Investments’ asset management team.

1The PPUT Index is the CBOE S&P 500 5% Put Protection Index, which tracks the value of the S&P 500 and a monthly 5% out-of-the-money put option. The SPXTR Index is the S&P 500 Total Return Index tracking the stock performance of 500 large companies listed on stock exchanges in the United States. In the SPXTR, changes in the index level reflect both movements in stock prices and the reinvestment of dividend income.

Past performance is not indicative of future results. Options are not suitable for all investors and carry additional risks. Options may not perform as intended and could expose an investor to losses, e.g., option premiums, to which it would not have otherwise been exposed.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry, or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice, or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments.

The investments recommended by Horizon Investments are not guaranteed. There can be economic times when all investments are unfavorable and depreciate in value. Clients may lose money.

Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns. Low-volatility investing is not a guarantee against loss or declines in the value of a portfolio. All investing involves risk of loss, and in periods of market growth, risk mitigation strategies can be expected to lag in performance behind equity strategies that do not focus on risk mitigation.

This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent. Forward-looking statements cannot be guaranteed.

References to indices or other measures of relative market performance over a specified period of time are provided for informational purposes only. Reference to an index does not imply that any account will achieve returns, volatility, or other results similar to that index. An index’s composition may not reflect how a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, restrictions, sectors, correlations, concentrations, volatility or tracking error targets, all of which are subject to change. Individuals cannot invest directly in any index.

Other disclosure information is available at hinubrand.wpengine.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2023 Horizon Investments LLC