Stock investors may want to brace for some bumps in the road.

After months of gains and low volatility from stocks, emerging signs show that supportive equity

trends are taking a pause, and the market could experience some chop in the coming weeks.

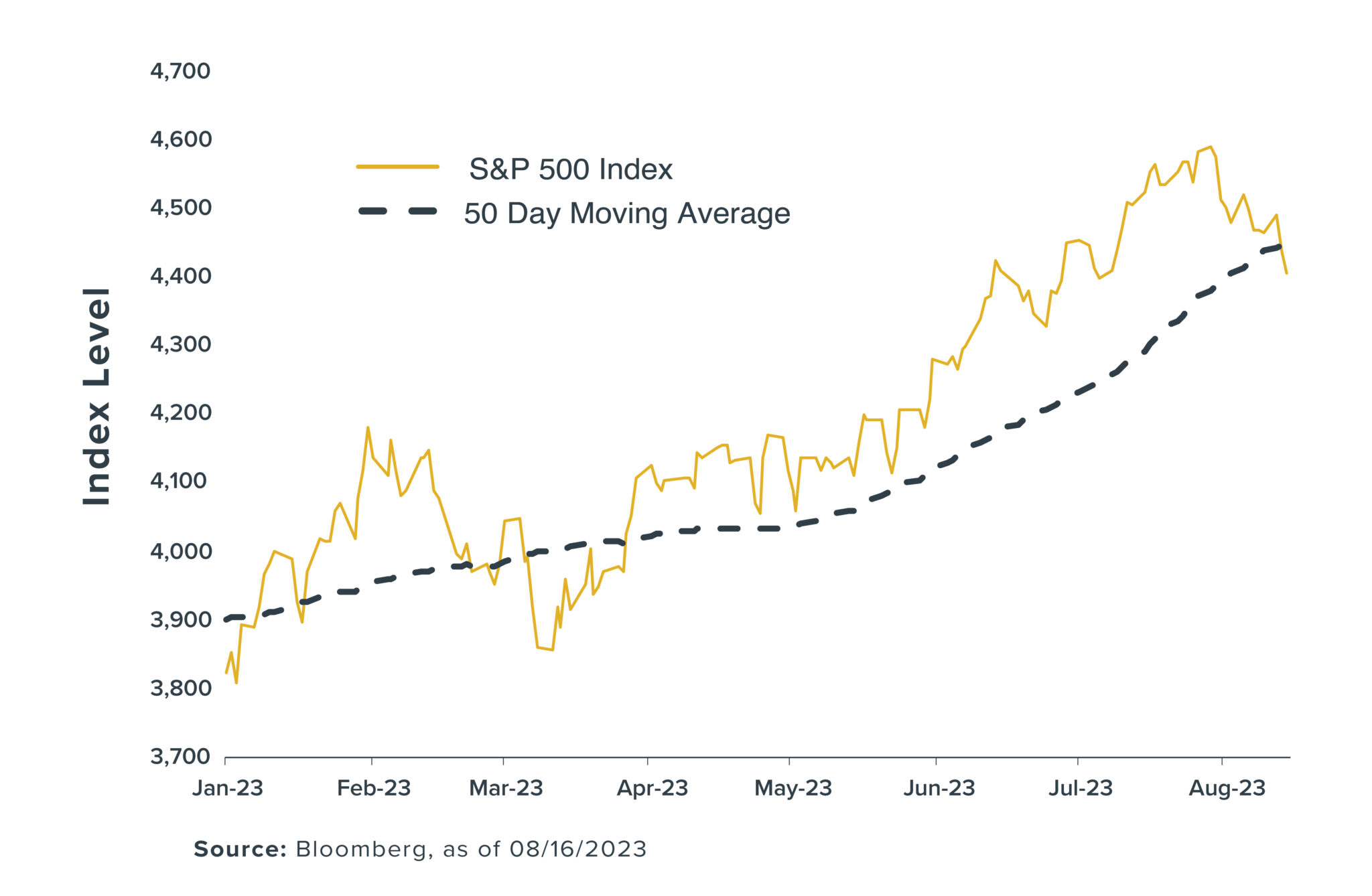

This week, for example, the S&P 500 closed at its lowest level since July 11 and dipped below its

50-day moving average1 (a gauge of market momentum) for the first time since late March, as shown in the chart below.

Until this week, the S&P 500 had closed above its 50-day moving average for 95 consecutive sessions—the index’s longest run since a 102-session streak ended in September 2020.

The recent downward pressure on stocks could intensify in the coming weeks, particularly if further weakness prompts large systematic investors—who use moving averages and other quantitative data to adjust their portfolios—to head for the exits. More negative economic news from China or unwelcome comments from central bankers at next week’s Jackson Hole Economic Symposium could be catalysts to push stock prices lower.

Compounding that potential risk: Many of these systematic investors have steadily increased their stock exposure over the past year. For example, one systematic index’s2 equity allocation is the highest since December 2021. At its current level, $1 of exposure to this index has more than $1 of exposure to equities.

It’s not uncommon for stocks to suffer a late-summer slump. According to Dow Jones data, September has historically been the worst month for S&P 500 performance. Although numerous other factors remain supportive of stocks, don’t be surprised if there are further pullbacks before the market regains its upward momentum.

1 The S&P 500® 50-day moving average is the average price over the past ten trading weeks.

2 The S&P 500® Low Volatility Daily Risk Control 10% Index represents a portfolio of the S&P 500 Low Volatility Index plus an interest accruing cash component. The index is dynamically rebalanced to target a 10% level of volatility. Volatility is calculated as a function of historical returns.