Tactical investment strategies shift allocations in a portfolio to take advantage of shorter-term market opportunities with the goal of improving the trade-off between risk and reward. Similar to how an athletic coach may elect to switch a game plan mid-match to address the opposing team’s strengths and weaknesses, a tactical investment manager may adjust their portfolio exposures to seek a desired outcome. Compared to more passive or strategic investing styles, tactical strategies are typically more active and often feature larger and more frequent portfolio changes.

Figure 1 shows the spectrum of common asset allocation investment styles. Advocates of passive investing believe that the stock market is unpredictable, and therefore the best portfolio makes no changes in response to market information. By comparison, active strategies account for market conditions by adjusting the portfolio’s holdings over time. Strategic approaches to active management may maintain consistent portfolio tilts or change slowly over time, while tactical approaches respond more quickly to market information.

Figure 1: The spectrum of passive and active strategies.

Seeking Opportunity with Tactical Management

Tactical implementations may vary significantly from manager to manager. Two of the most common types of tactical strategies occur within asset classes and across asset classes.

Tactical Allocation Within an Asset Class

Tactical allocation within an asset class begins with setting a strategic asset allocation, and then adjustments are made to the holdings within the specific asset classes, in an effort to take advantage of market trends or opportunities. Allocation adjustments in this context are typically applied to broad baskets of stocks that share similar characteristics but may respond differently to various market conditions.

These characteristics may include the following:

- Geography – US or international stocks

- Style – high-growth or low-growth companies

- Size – large, mid, and small-cap companies

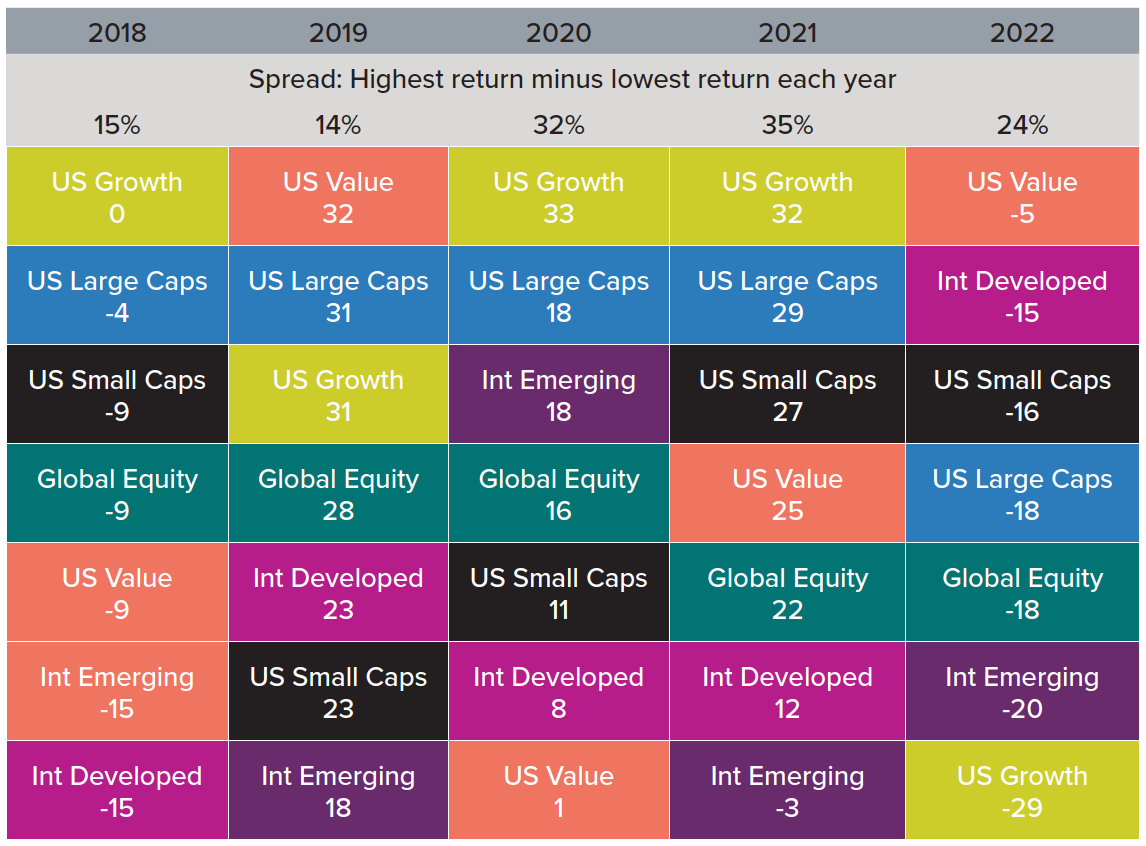

Figure 2 shows the performance differences between equity allocations over the last five years. Even within such a short time frame, there has been considerable variation in the annual spread of returns ranging from a low of 13% in 2019 to a high of 35% in 2021. While large spreads introduce the risk of underperformance, they also represent a potential opportunity for effective tactical managers.

Figure 2: A chart of broad global equity factors from 2018 through 2022.

Source: Indices from Bloomberg, calculations by Horizon Investments. Global Equity is the MSCI Global Index, Int Developed is the MSCI Ex-USA Index, Int Emerging is the MSCI Emerging Markets Index, US Value is the S&P 500 Value Index, US Growth is the S&P 500 Growth Index, and US Small Caps is the S&P 600 Small Cap Index. It is not possible to invest directly in an index. Please see attached disclosures.

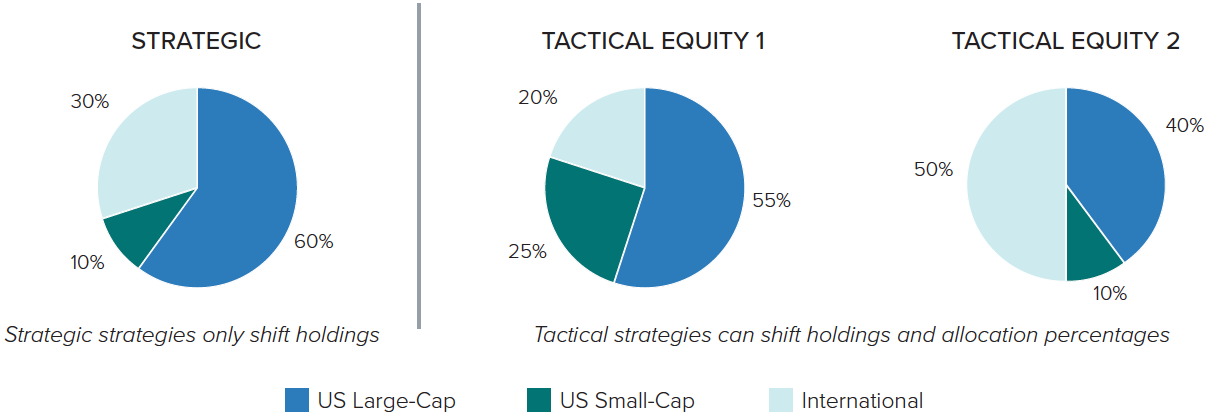

Figure 3 shows an example of the differences in activity over time between a strategic and tactical approach. For the purpose of this illustration, the strategic allocation does not change exposures. However, for tactical strategies within an asset class, the manager may adjust the allocation to each equity component based on market conditions while keeping the overall stock or bond allocation the same.

Figure 3: Illustrative example of exposure changes of tactical and strategic allocations.

Source: For illustrative purposes only by Horizon Investments. Not representative of any specific account.

Tactical Allocation Across Asset Classes

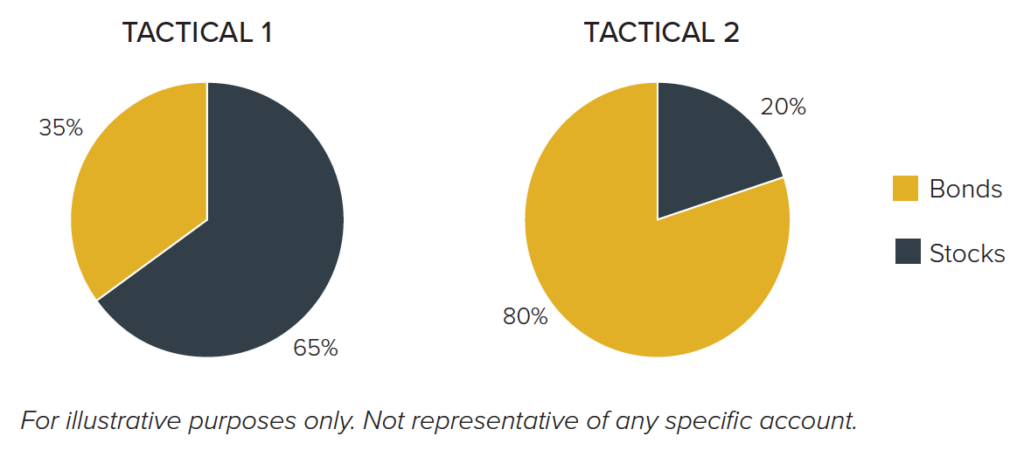

In contrast, tactical allocation across asset classes means the proportions of the portfolio allocated to stocks, bonds, or cash are expected to change over time depending on market activity. Because allocations can greatly vary, these strategies typically display a broader range of risk and return expectations than tactical allocations within an asset class.

For example, a tactical strategy may shift allocations across stocks and cash with the goal of adjusting the exposure to equities within certain risk limits. Therefore, if stocks go down in value or otherwise risk increases, the proportion allocated to stocks may be reduced in an attempt to minimize further losses.

Figure 4 shows an example of the active change in exposure to stocks and bonds that a tactical manager may make in response to market conditions. Notice that the stock and bond allocation changes dramatically over the two periods, which may have a larger impact on strategy expectations than adjusting allocations within an asset class.

Figure 4: Illustrative example of tactical allocations.

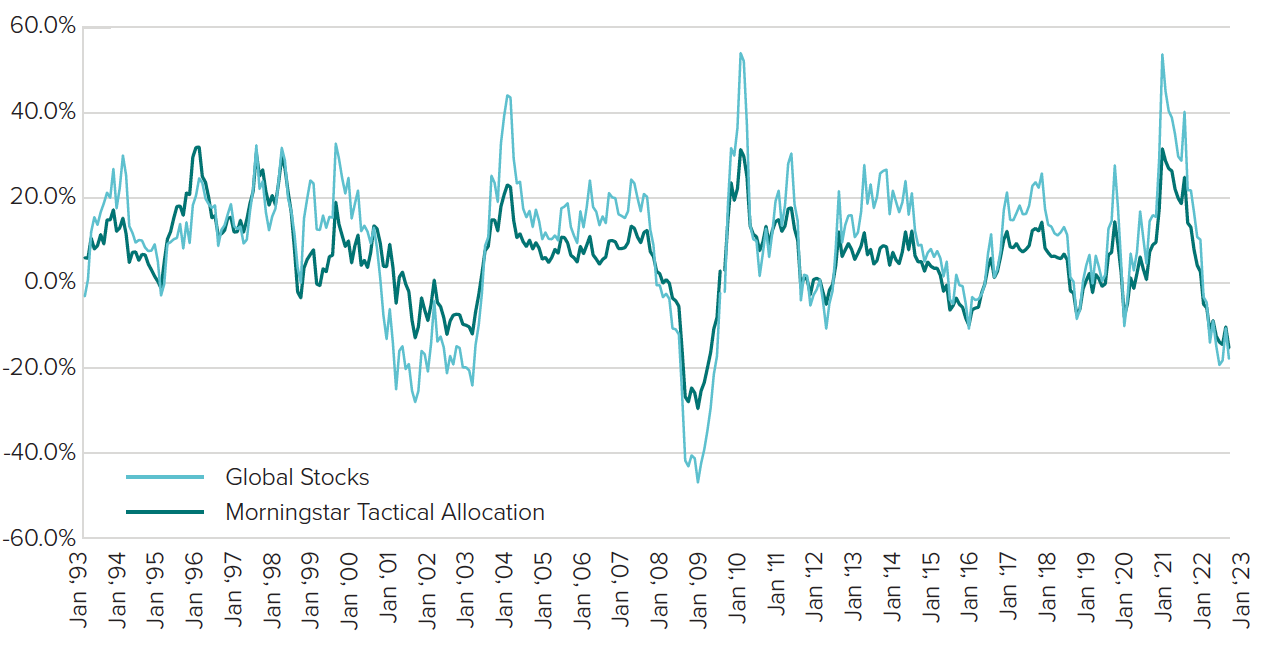

Figure 5 compares the Morningstar Tactical Allocation category to broad global stocks (represented by the MSCI World Index). The lower volatility of the tactical allocation, represented by the darker line, is apparent – maximum gains and drawdowns are both smaller than they are for global stocks. Tactical allocation strategies come in many different shapes and sizes; therefore, we believe managers must be transparent about their specific approach to create consistency in expectations.

Figure 5: Rolling annual returns of Global stocks and Tactical Allocation

Source: MSCI World Index and Morningstar Tactical Category over the last 30 years from 1993 – 2022, calculations by Horizon Investments. It is not possible to invest directly in an index. Please see attached disclosures.

Tactical Allocation within Horizon’s Goals-Based Framework

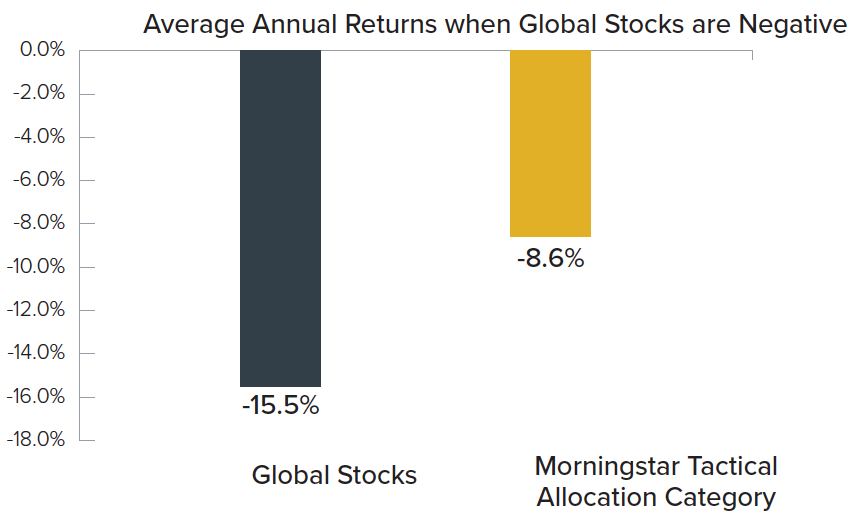

Horizon’s Goals-Based Philosophy has been developed and refined after years of practical experience working with advisors across different market environments. We focus on providing investors with investment solutions that align with their financial plans. Although past performance is not an indicator of future results, tactical strategies, both within and across asset classes, have historically performed better, on the downside, than strategic strategies when returns were highly dispersed or when markets exhibited above-average volatility (as shown in Figure 5). Those two conditions often coincide with market downtrends, and Figure 6 shows that, on average, tactical strategies have outperformed global stocks during years when stock returns are negative. And as many investors have experienced, volatile and difficult market environments can lead to investment behaviors that may disrupt an investment plan.

Figure 6: Downside performance of the Morningstar tactical allocation category verses global stocks

Source: MSCI World Index and Morningstar Tactical Category over the last 30 years from 1993 – 2022, calculations by Horizon Investments. It is not possible to invest directly in an index. Please see attached disclosures.

Because of the potential for tactical strategies to reduce risk when needed and thereby improve an investor’s experience, Horizon views them as core features of an effective goals-based investment solution. Horizon deploys tactical strategies within our design of goals-based portfolios in two distinct ways.

- Accumulation: For clients with an accumulation objective and a long investment horizon, we believe tactical allocation within an asset class may be appropriate because of its ability to respond to changing market environments while keeping the long-term desired asset allocation intact.

- Preservation and distribution: For clients with a primary objective of preservation or distribution, and a shorter investment horizon, we believe tactical allocation across asset classes may be appropriate since it can provide a greater degree of risk mitigation.

In either case, tactical strategies can also be blended with more strategic or passive choices to further enhance diversification across investing styles, as different types of markets may favor one approach over the other.

Horizon believes tactical strategies can offer the flexibility to more accurately customize portfolios to meet investors’ needs and seek long-term investment objectives.