The Federal Reserve giveth, and the Federal Reserve taketh away. What was a saving grace for the stock market in March and April 2020 – the use of zero-interest rate policy – has turned into a curse in January 2022. Jay Powell and his colleagues at the central bank are ready to rip off the emergency, easy-money band aid amid a roaring economy, tight labor market and skyrocketing inflation. And as that realization sinks in, market participants are abandoning the riskiest, highest-flying investments, from pandemic darling stocks to cryptocurrencies to meme stocks. Horizon expects this bout of market volatility to continue in the near-term as investors process the implications of tighter monetary policy from the Fed.

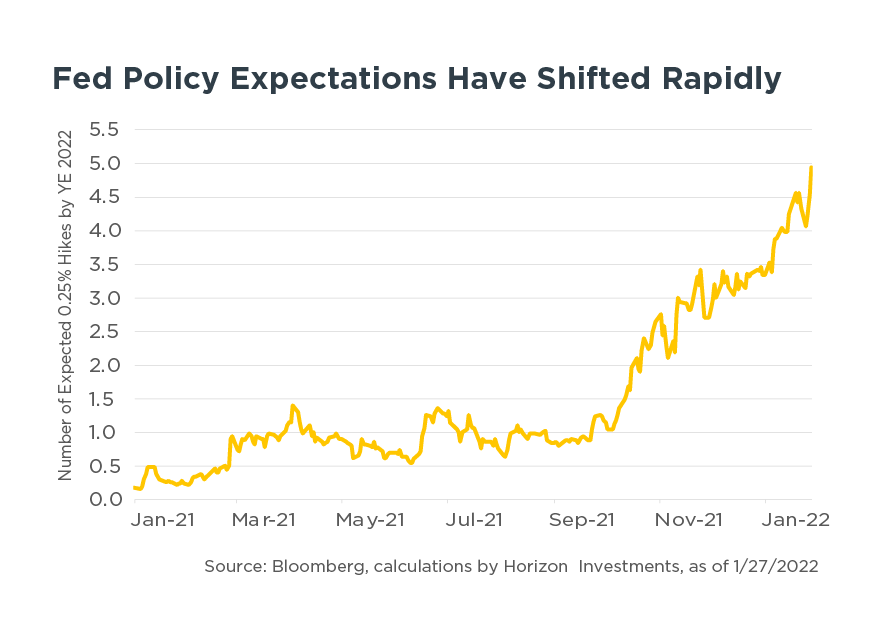

The abrupt shift in Fed policy – from easy to an increasingly tighter stance – has reintroduced volatility to markets. What drove the shift? Inflation. Instead of inflation easing into the back half of 2021, it picked up steam. There are good arguments on both sides of the inflation outlook (see our Q4 Focus for a deeper dive). Goods’ prices have experienced strong price pressures, and this has broadened out recently; a combination of continued supply chain pressures, higher energy prices, and some pass-through of wages are key drivers. On the other hand, higher interest rates and the end of stimulus checks may put a chill in consumer shopping and bidding wars for homes. The Fed, like many other market participants, has been caught off guard by the current high-inflation dynamics. That has forced the central bank to become more “nimble,” in Chair Powell’s words, and to communicate that they will move hard and fast to restore price stability and rebuild their credibility as an inflation fighter.

How did we get to this week’s market gyrations? The Fed relied on their forecasts that inflation would come down – the same forecast that many market participants had – and it turned out to be wrong (at least in 2021). By pivoting to a more flexible, data-dependent approach, they essentially conceded that the idiosyncratic changes to the economy during the pandemic and the incredibly fast nature of this recession to recovery cycle have hampered their ability to predict the future path for the economy. According to the Fed’s newly held view, in today’s environment acting on forecasts could hurt more than it could help. And with inflation currently at 40-year highs, it appears the Fed now believes that it may have to move very aggressively to stamp it out.

In the stock market, ripping off the easy-money band aid certainly hurts, and investors are in the process of separating the wheat (the major indexes) from the chaff (the high momentum areas). Witness the dizzying corrections for The Bloomberg Galaxy Crypto Index – down over 50% from its November 9, 2021 high and the IPOX SPAC Index – off 44% from its high last February to January 27, 2022. The average stock in the Nasdaq Composite Index has experienced a decline of about 47% from its peak, according to a JP Morgan report on January 25, 2022. The aforementioned market sectors are all essentially speculative plays – all valuation and sentiment and little to no earnings.

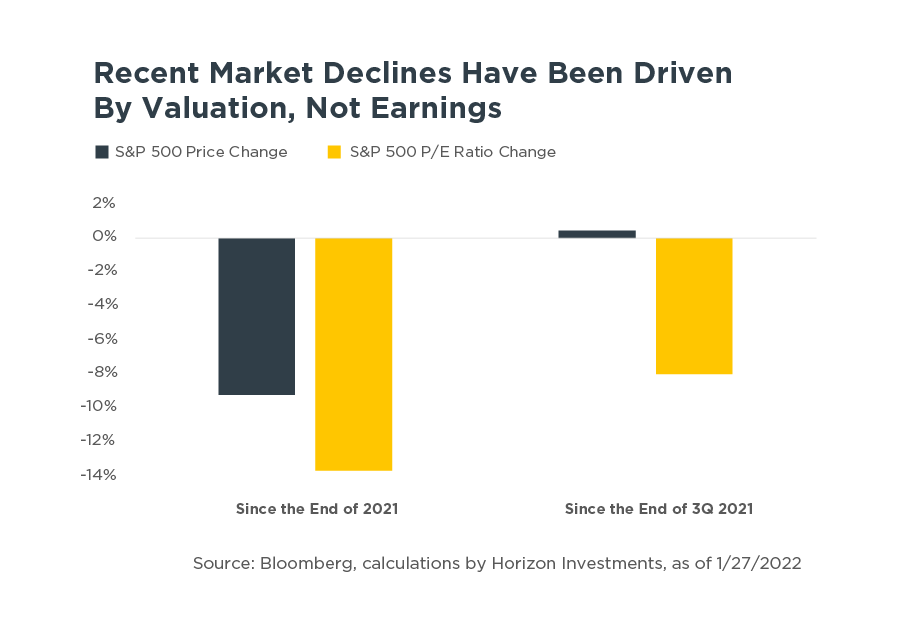

Viewing stocks through the lens of price-to-earnings multiples (P/Es) – a common equity valuation metric – helps put the recent decline of broad market indices in context. The S&P 500 Total Return Index is down about 10% from its peak on January 3, 2022. As seen in the chart below, its recent declines have been driven by a fall in valuations, not earnings – since the start of the year, the Bloomberg consensus earnings expectations for the S&P 500 Index have actually risen. Stock prices have fallen recently due to a re-rating of valuation multiples as the Fed’s hawkish pivot introduces higher risk and uncertainty, not as a result of falling earnings. Our point is that equity fundamentals remain robust, and the core of the stock market is much more resilient than the ostentatiously frothy areas.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments. Index information is intended to be indicative of broad market conditions. The performance of an unmanaged index is not indicative of the performance of any particular investment. It is not possible to invest directly in an index.

Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent.

Other disclosure information is available at hinubrand.wpengine.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2022 Horizon Investments LLC