¹Assumes the portfolio will be tax-advantaged, that there’s a 30-year time horizon with a zero portfolio balance at the end, that the portfolio will be annually rebalanced, and that the retiree will make annual midyear withdrawals.

The chart above highlights a Monte Carlo simulation study from Horizon published in the research paper, “The Retirement Income Challenge” (June 21, 2023). Asset returns are assumed to be normally distributed with given means, volatilities, and correlations. Our base case assumes conservative estimates for future returns in line with those referenced by Morningstar Benz et al. (2021). Specifically, we assume that stocks return 8% per year (equal to the average return of global stocks over the last 30 years as of 12/31/22), bonds return 4% per year (in line with current yields and average bond returns over the last 30 years as of 12/31/22), and inflation is 2.5% per year (equal to the average of short-term and long-term breakeven inflation expectations as of 12/31/22).

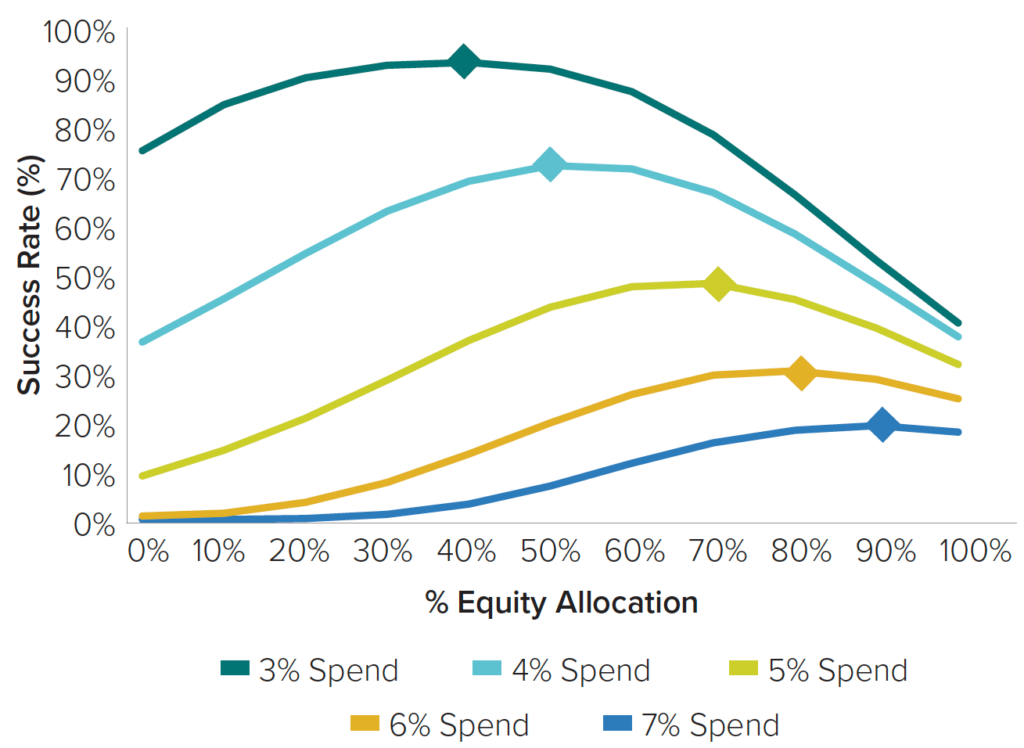

Optimal stock and bond allocations for risk-optimized spending strategies (ROSS) Distribution Rate | 3% | 4% | 5% | 6% | 7% |

Stock (%) | 40% | 50% | 70% | 80% | 90% |

Bond (%) | 60% | 50% | 30% | 20% | 10% |

Correlations are, on average, zero (the long-term correlation between broad stocks and bonds). Volatility is assumed to be 16% per year for stocks and 5% per year for bonds, consistent with volatility estimated over the last 30 years as of 12/31/22. We simulate 10,000 paths averaging results across all periods. An initial cash distribution is defined as a percentage of the total portfolio value and is taken at the beginning of each period described in the study; distributions are also adjusted upward for inflation at the end of each year. We simulate planning horizons of 20, 25, and 30 years to match the life expectancy of either or both individuals from a married 60-year-old couple as estimated by the longevity illustrator maintained by the Society of Actuaries as of 12/31/22. To account for practical frictions, we assume a management fee of 1% taken as a percentage of the portfolio at the beginning of each period described in the study and a long-term capital gains tax rate of 15%. We do not take into account custodial or brokerage fees, which would have the effect of reducing returns. The simulation does not represent actual performance. This simulation is not replicable of any specific Horizon portfolio or strategy but is rather an allocation of fixed assumed asset classes.

For the chart, we used a standard withdrawal study to define an optimal asset allocation and compared it to other typical retirement spending portfolio solutions for our analysis. We assumed an initial distribution rate that increased with inflation each year after that from a portfolio of stocks and bonds. We simulated returns using conservative capital market assumptions and accounted for taxes and fees. Our core metrics were: 1) A success rate is the percentage of simulated paths where all desired distributions are achieved. 2) Real

legacy wealth, or the wealth that remains, is defined as the average inflation-adjusted ending values as a percentage of the starting portfolio values.

For additional information regarding this research, please contact Horizon at info@horizoninvestments.com.

The Real Spend® retirement income strategy is NOT A GUARANTEE against market loss and there is no guarantee that the Real Spend® strategy chosen by an investor will be successful for the entirety of an investor’s retirement. Clients may lose money. Real Spend® is an asset allocation strategy that uses an investment model to (i) plan savings amounts and overall asset allocation during the distribution phase of retirement planning, (ii) compute target retirement wealth, assuming a retirement budget and a spending-investment strategy after retirement, (iii) compute the transition from the accumulation phase to the retirement phase, and (iv) generate the spending-investment strategy after retirement. Our retirement spending investment strategy uses an allocation model that replenishes cash needed for withdrawals. Before investing, consider the investment objectives, risks, charges, and expenses of the strategy. All investing involves risk. This strategy is not an insurance product with payments guaranteed. It is a strategy that invests in marketable securities, any of which may fluctuate in value. There is a possibility of outliving the assets if market performance is lower than forecasts used in planning, or if longevity is longer than anticipated. Calculations used with investors are estimates based on historical market behaviors, and there is no assurance that these behaviors will be repeated in the future. Investors should note that historical data suggests that higher Spend Rates will have a lower likelihood of success for the entirety of the retirement period than a lower Spend Rate would. Past performance and market data are no guarantee of future results and investor experiences will vary.

This commentary is written by Horizon Investments’ asset management team. Past performance is not indicative of future results. Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry, or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice, or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments. Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns. All investing involves the risk of loss.

The investments recommended by Horizon Investments are not guaranteed. There can be economic times when all investments are unfavorable and depreciate in value. Clients may lose money. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. The opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent. Forward-looking statements cannot be guaranteed. Other disclosure information is available at hinubrand.wpengine.com.