It’s been bleak days—and lots of them—for bond investors.

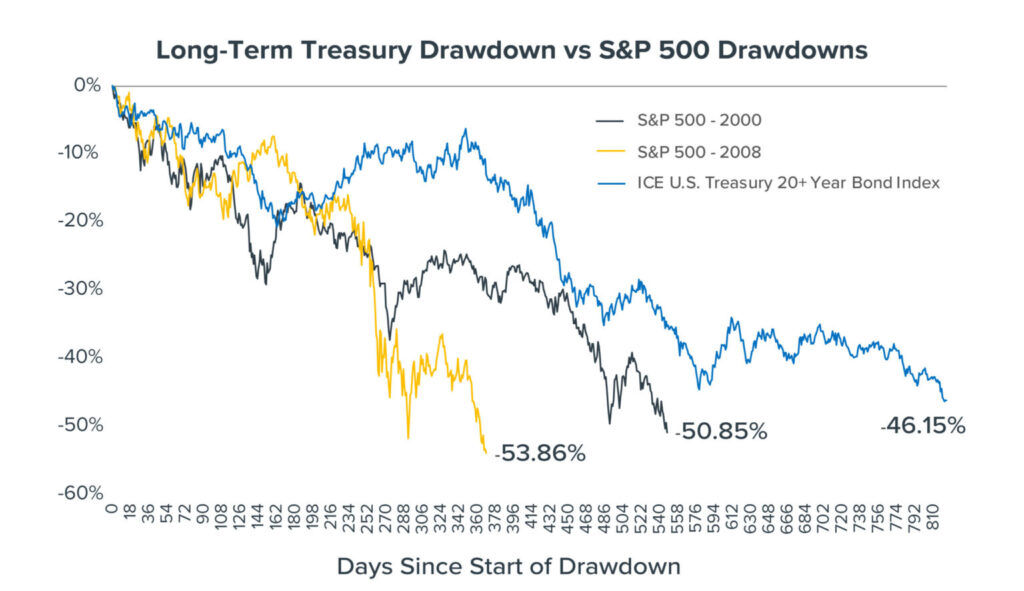

As the fourth quarter begins, bonds are on track for a third consecutive calendar year of losses—an unprecedented outcome, should it come to pass. Long-term Treasury bonds’ slog lower has lasted a whopping 823 trading days (as of 9/29/23), as rising rates have pummeled fixed-income investors with a -46.14% total return over that time (see the chart).

Amazingly, this current bond drawdown has lasted longer than the stock market slides of 2000 to 2002 (when the tech bubble burst) and 2008 to 2009 (the global financial crisis)—with a return nearly as bad as we saw in both bear markets.

The path to higher interest rates that we’ve been on has caused significant pain for many bond investors. There is some good news, however:

- When rates peak—and we may be there or close—the economy and stocks may be set up for success. Keep in mind that the long-term drivers of equilibrium interest rates are inflation and economic growth, and increases in productivity primarily drive growth. Therefore, we see falling inflation coupled with rising bond yields potentially as a healthy sign incentivizing more productive investment.

To see what that could mean, consider that the 10-year Treasury’s yield averaged 6.65% and inflation averaged 3% during the 1990s—a decade that saw the S&P 500 deliver an 18.2% annualized return. - With rates much higher than a few years ago, longer-duration bonds look relatively attractive. Example: Aggregate bonds today yield around 5.4%, with a duration (interest-rate sensitivity) of approximately six years. If rates rise by one percentage point over the course of a year, those bonds’ total return would be just below 0%. But a one percentage point drop in rates would result in a nearly 12% total return.

From an asset allocation perspective, exposure to short-duration bonds has paid off well in recent years. However, as rates have increased, the risk-return tradeoff has begun to shift in favor of longer-term bonds—a development we are watching closely within our core bond positioning.