Investors sure are a gloomy bunch these days.

How downbeat are they? According to the AAII Investor Sentiment Survey1 (a weekly

poll measuring individual investors’ outlook for the equity market), for the week ending

3/16/2022, investors’ bearish sentiment—the outlook that stock prices will fall over the

next six months—rose to 49.8%, versus its historical average of just 30.5%.

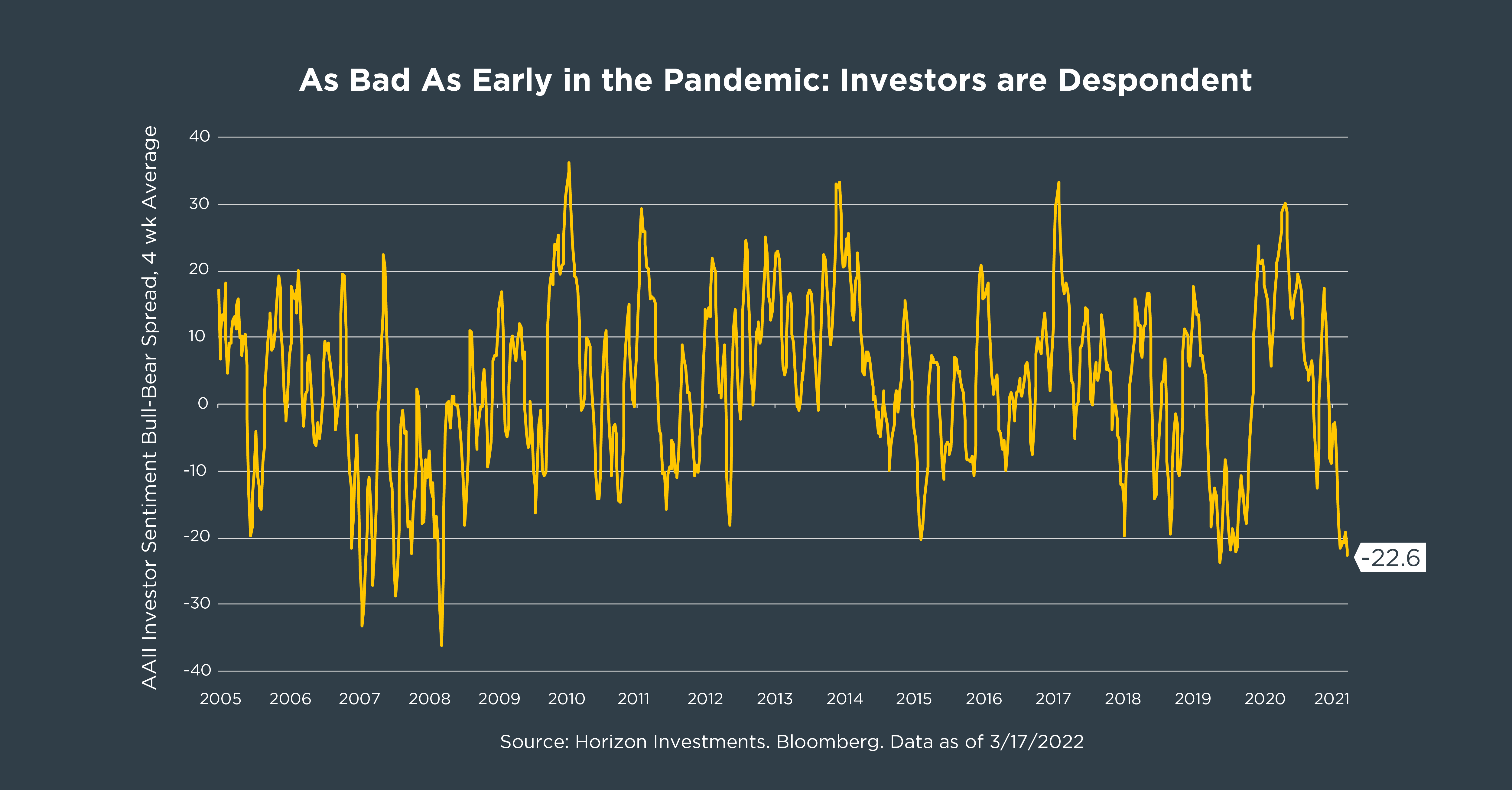

Even more telling: The gap between bullish sentiment and bearish sentiment—known

as the bull-bear spread—clocked in at a shockingly low –22.6 percentage points (on a

4-week moving average basis), as seen in the chart.

Notice that the last time investors saw a 4-week spread that dipped below -20

percentage points was shortly after the pandemic started—and you have to go all the

way back to the 2007-2008 global financial crisis to find a larger negative spread!

So it might surprise your clients to learn that all this negativity could mean good things

for their wealth—if they’re positioned properly.

The reason: Historically, stocks have rallied after investor sentiment turned south.

Following periods when the bull-bear spread was -10 percentage points or more (on a

4-week moving average basis), the S&P 500 on average posted the following returns:

● 8 weeks out: 3.4%

● 12 weeks out: 5.1%

● 52 weeks out: 15.5%

We believe the recent extremes in investor sentiment help to put stock market

performance of late—such as the S&P 500’s 6.1% rally last week—into context. The

shock to valuations stemming from the rapid changes in Fed expectations has clearly

hurt sentiment. As a result, stock prices have corrected lower for much of 2022.

But investors have now appeared to digest these changes, which likely means the worst

is behind us. However, that benign scenario rests on the idea that both economic and

corporate fundamentals must remain healthy.

We will be watching carefully to see whether consumers continue to spend or instead

pull back consumption due to factors such as higher inflation and the Russian invasion

of Ukraine. Corporate earnings growth will be impacted largely by how consumers

respond going forward, and it’s worth noting that the market still foresees healthy

corporate earnings for the year.

Should the expected strength in corporate earnings come to fruition, it would support

investors’ use of equity allocations to meet long-term goals–particularly in an

environment of higher inflation and suppressed interest rates. However, the possibility

that consumers could potentially rein in their spending would make the case for risk

management strategies aimed at limiting drawdowns among investors who need to

access their funds in the near term.