Powell and co. are likely to sit on their hands for a while

Fed watchers may want to consider taking the summer off this year.

Federal Reserve Board members are likely to maintain their “wait-and-see” approach of the past few months, thanks to economic data showing little need for decisive monetary policy action in the near term. For example:

- Inflation is reasonable: The Personal Consumption Expenditures (PCE) Price Index rose 2.1% in April on an annual basis—the lowest rate since September—while the core inflation rate (which excludes the volatile food and energy categories, and is the Fed’s preferred measure of inflation) came in at 2.5%, the lowest level since March 2021. Both numbers are relatively close to the Fed’s target inflation rate of 2%.

- The job market is healthy: Although the labor market has softened recently, the number of new jobs added each month—139,000 in May, for example—remains strong enough to keep unemployment near historically low levels and prevent the Fed from having to shore up conditions through rate cuts.

- Tariff uncertainty remains high: It’s still unclear how President Trump’s widespread tariffs will play out and impact inflation and economic growth rates. Given this uncertainty, there is little incentive for the Fed to act.

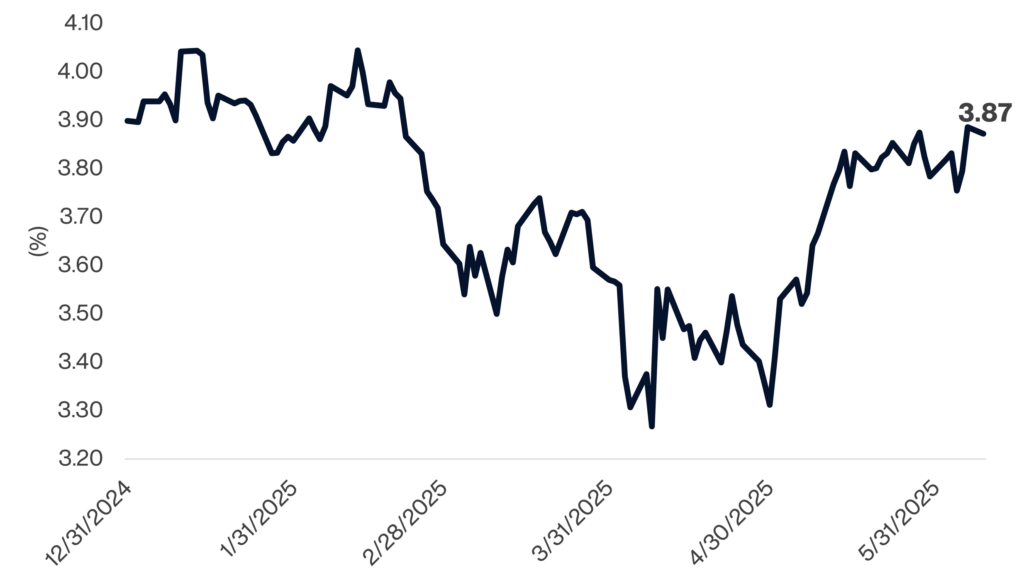

As a result, the current implied federal funds rate for December 2025 (derived from fed funds futures) is hovering right around where it began the year, roughly 3.9% (see the chart). Moreover, despite falling sharply when tariff-based risk was at its highest, the implied rate has barely moved over the past month.

Implied Federal Funds Rate in December 2025

Source: Bloomberg, calculations by Horizon Investments, data as of 6/9/25.

The upshot: Unless some truly surprising economic data comes out of left field, don’t expect drama when the Fed meets in June and July. For now, tariffs remain the story to watch.