It’s a game of “catch me if you can” between investors and the Fed these days.

For the most part, the Fed’s recent series of rate hikes has been trying to keep up with the market’s future expectations for interest rates—leading to concerns that the Fed is behind the curve in terms of where rates need to be to effectively fight inflation.

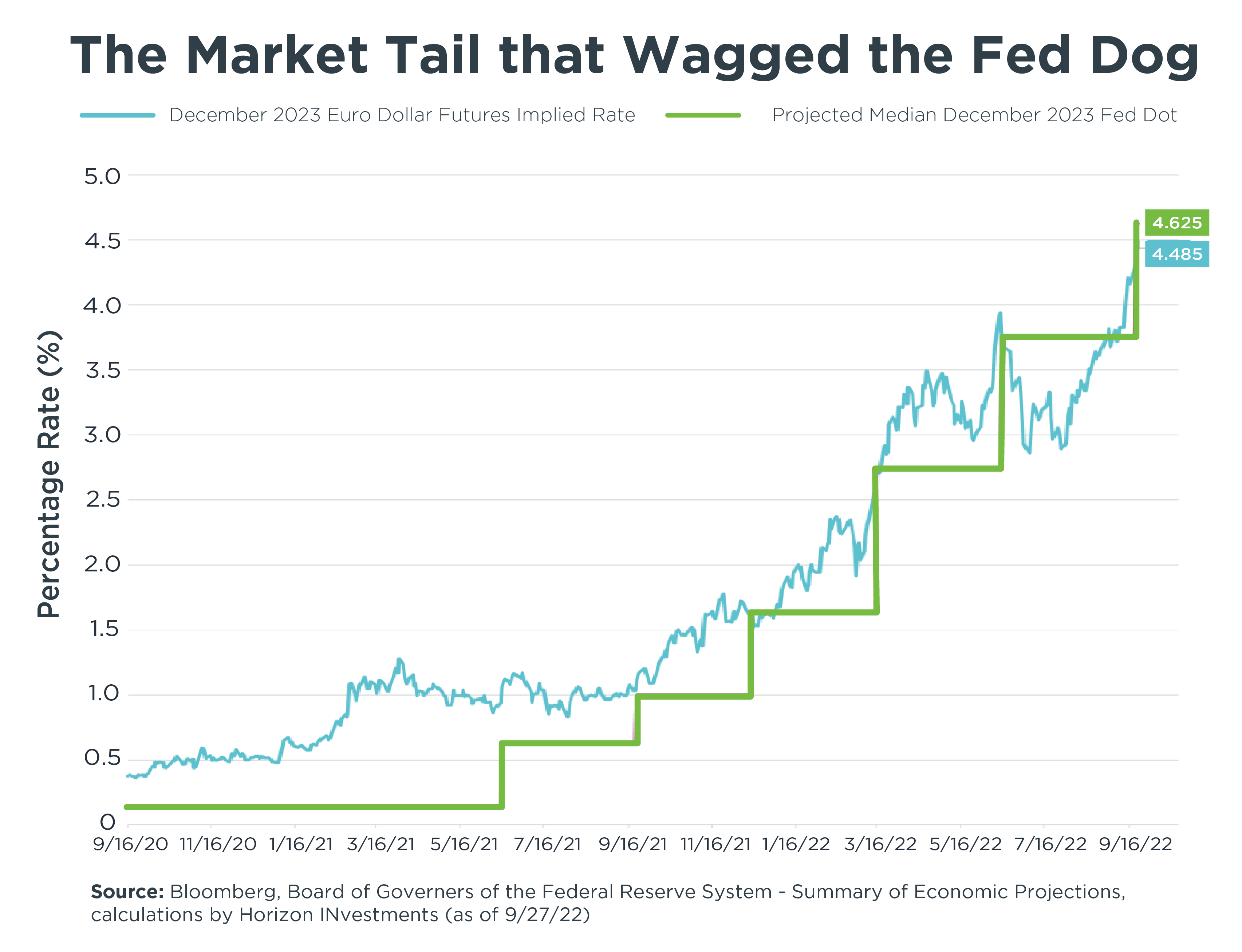

More recently, however, the market has been chasing the Fed.

As seen in the chart, Eurodollar futures, a good reflection of the market’s outlook for US interest rates over the next few years (the blue line) essentially led the charge in predicting higher rates. The Fed’s outlook for rates (their “dot plot,” shown in green) consistently lagged behind the market’s before eventually converging with it on four separate occasions.

That changed this summer when the market began eyeing the possibility of lower rates down the road. Investors cut their rate expectations to as low as 2.86% in July, driven partly by their prediction that the Fed would eventually need to cut rates to stimulate the economy.

As we all know, when it was time for the Fed to update its outlook, it did not follow investors lower. Instead, it raised its rate expectation significantly to 4.625%–citing factors such as anticipated lower real GDP growth, higher unemployment, higher inflation, and higher interest rates over the next few years.

Now it was the market’s turn to give chase: Futures shot steadily higher in August and September—and as of September 27, the market has caught up with the Fed, with the difference between their respective rate predictions a mere 0.14 percentage points.

The message is clear: Investors have woken up to the fact that the Fed means business in its fight against inflation—and that interest rates are not likely to come down any time soon. As we’ve noted in the past, we’re looking at a “higher, for longer” scenario–and the Fed and the market appear likely to track each other more closely going forward.

Until we see a meaningful decline in the trend in inflation, we expect continued market volatility and a challenging environment for asset valuations.

This commentary is written by Horizon Investments’ asset management team.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances that may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Horizon Investments, LLC (“Horizon”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security in question is suitable for their particular circumstances and, if necessary, seek professional advice. Investors may realize losses on any investments.

Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed herein are our opinions as of the date of this document. These opinions may not be reflected in all of our strategies. We do not intend to and will not endeavor to update the information discussed in this document. No part of this document may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without Horizon’s prior written consent. Forward-looking statements cannot be guaranteed.

Other disclosure information is available at hinubrand.wpengine.com.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC

©2022 Horizon Investments LLC