Investors typically regard bonds as a safe haven because of their reputation for having lower risk and lower return profile. For investors preparing for retirement, or those already in retirement, a common rule of thumb has been to shift away from equities into bonds. The phrase “own your age in bonds”, however, may need to be reconsidered in today’s market environment.

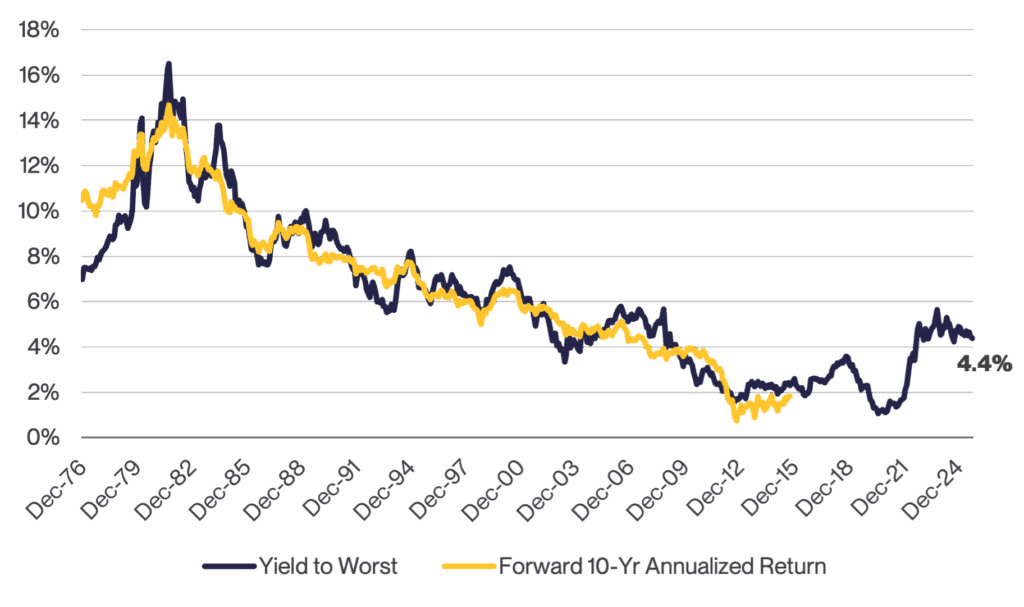

Sharply rising inflation in 2022 reminded investors that bonds are not always low-risk, as fixed income suffered steep losses. In the short term, they can sometimes lose a significant amount of money. The question now is what today’s data tells us about bonds’ role going forward. By examining yields, diversification benefits, and income potential, we can better understand how to position bonds and related strategies in today’s bond market. Chart 1 below illustrates that today’s yields can be an excellent predictor of future returns.

CHART 1: CURRENT YIELD VS. FORWARD 10-YEAR RETURNS FOR INVESTMENT GRADE BONDS

Bloomberg Aggregate Bond Index

Bloomberg U.S. Agg Total Return Value Unhedged USD Index (LBUSTRUU) (bonds) from Bloomberg, December 1976 through September 2025, calculations by Horizon. Past performance is not indicative of future results. It is not possible to invest directly in an index. Please see attached disclosures.

Turning to diversification benefits, Chart 2 shows the rolling five-year stock and bond correlation at 0.6, the highest level on record over this period, as of September 2025. The prevailing level of inflation is a key factor driving correlations between stocks and bonds. These asset classes tend to exhibit negative correlations when inflation is roughly below 3%, such as during the years 2000 to 2021. Since the mid-1970s (except for the early 2000s), bonds have generally moved in step with stocks, especially during periods of elevated inflation.

CHART 2: ROLLING 5-YEAR STOCK AND BOND CORRELATIONS

Bloomberg U.S. Agg Total Return Value Unhedged USD (bonds) index and S&P 500 index (stocks) from Bloomberg, December 1976 through September 2025, calculations by Horizon. It is not possible to invest directly in an index. Please see the attached disclosures.

According to the New York Fed’s survey of consumer expectations, the median 1-year inflation outlook currently sits at 3.4%, while the University of Michigan’s 5-10 year longer-term survey has expectations at 3.7%. Persistently high inflation is arguably likely to remain, which could limit the ability of bonds to provide diversification.

Finally, turning to income potential, Table 1 compares yields across bonds, U.S. Treasury bills, and dividend stocks. A flat yield curve has left short-term Treasury bills offering income comparable to many bonds, while dividend-oriented equities, having largely missed the Artificial Intelligence-driven market rally, continue to provide relatively attractive yields. Taken together, both cash and dividend stocks deliver similar income potential to bonds, but without the same interest rate risk.

TABLE 1: ESTIMATED INDEX YIELD OF BONDS, CASH, AND DIVIDEND STOCKS