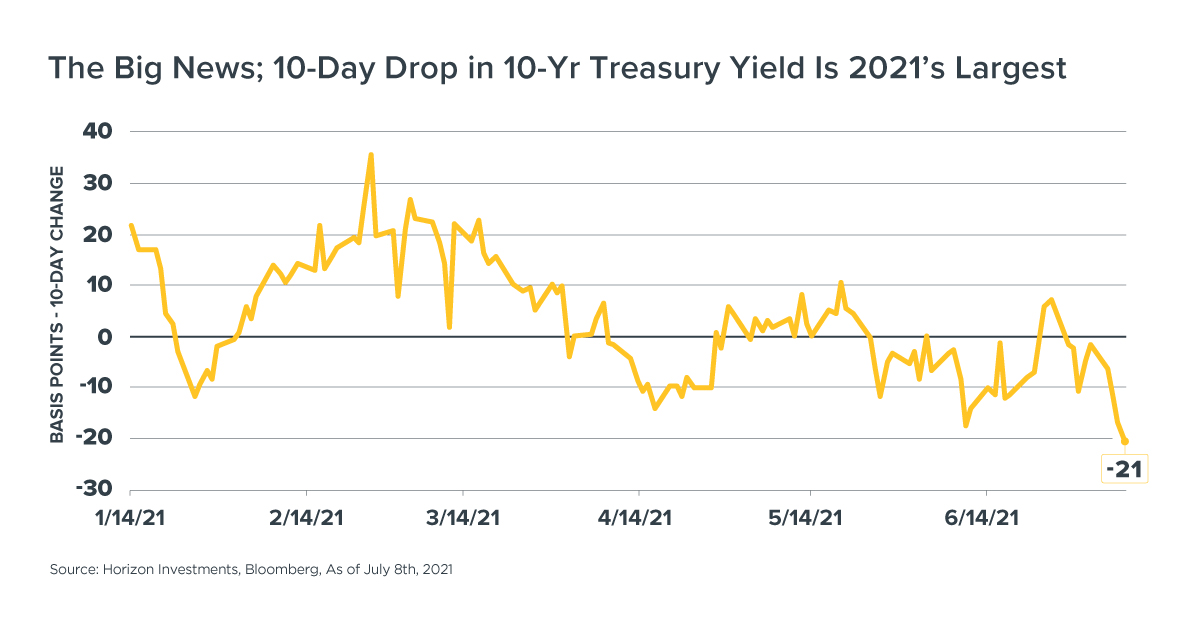

There’s no one, clear catalyst to point to for the rapid drop in yields. And that uncertainty spilled over into stocks as perplexed traders decided to take a more conservative stance until more is known. The S&P 500 fell at the opening bell, but quickly recouped part of the loss.

Such large moves in bonds in a short period of time can sometimes take on a momentum of their own as traders who were hoping for a reflation trade are forced to get out of the way. That can produce exaggerated moves as traders manage their risk. At this point, no one can rule out more volatility and big headlines as investors re-position in the wake of the bond market rally.

What’s the Catalyst?

Any number of reasons have been cited for the action. One firm, Deutsche Bank, conducted a poll of 300 investors and traders and listed the drivers from most to least important, reports Bloomberg News.

- Supply and demand technicals

- Secular stagnation/growth scare

- Federal Reserve potential pivot towards removing stimulus

- Covid/Delta variant concerns

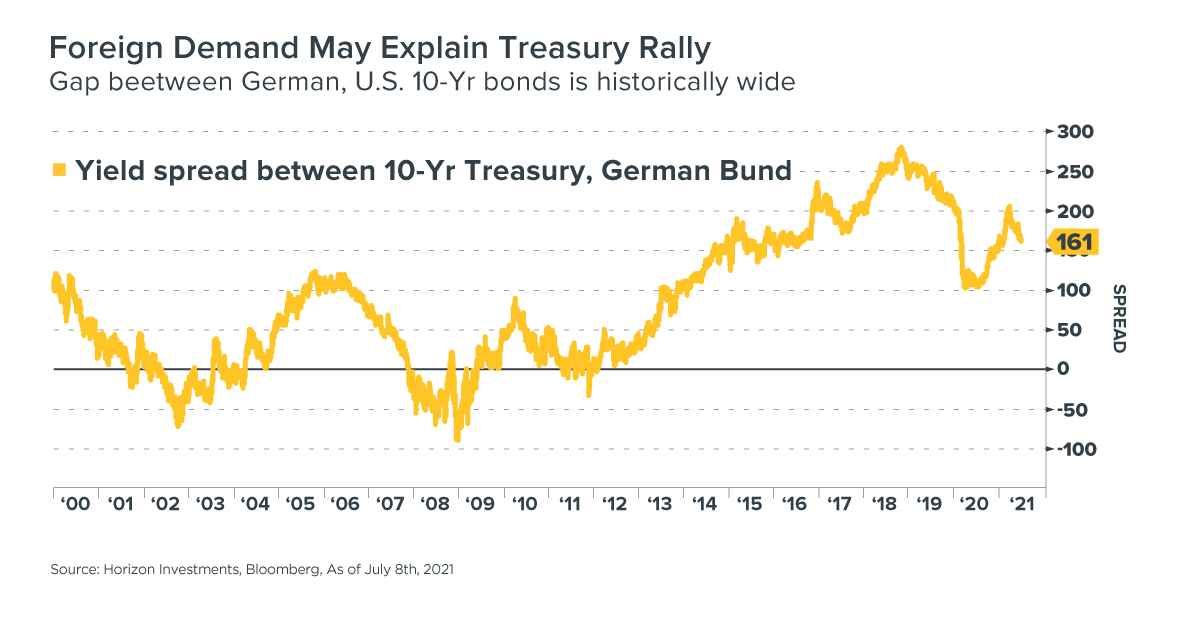

Demand for Treasuries has been strong despite the record size of recent auctions. Foreigners are likely attracted to the high yields on offer in the U.S. compared to their home market. For example, the 10-year Treasury currently yields 161 basis points more than its German counterpart. That’s still near this year’s high, and is among the widest spreads since the turn of the century.

Turning to the Federal Reserve, two changes have occurred recently that may be playing a role in bond volatility.

- This week’s release of the minutes of the central bank’s June meeting showed a few officials thought the time to remove some bond-buying support might be getting closer given the strength of the U.S. economy.

- The so-called dot-plot released at the last meeting showed a shift towards a potentially earlier increase in interest rates – moving it up a year to 2023. Horizon wrote about that news on June 24, noting that abnormally low interest rates would likely still be the case for several more years.

Put together, the two changes and the ongoing public debate among Fed officials about what to do about bond-buying and rates may have caught off guard people who were expecting the central bank to let economic growth and inflation run hot for years to come.

As for Covid and the rise of the more contagious Delta variant, the concern about new economic restrictions is gaining traction.

Japan has just announced that it will not allow any spectators to attend the Olympic Games due to a sudden rise in infections. Japan and other Asian countries have much lower vaccination rates than the U.S., raising the risk that more health protection measures may be put in place and global supply chains might be disrupted. Indonesia may be the next hot spot after India’s recent troubles.

On a global basis, however, the Covid case count is stable and the number of deaths is tumbling. In the United Kingdom, where cases are rising sharply due to Delta, mortality remains low. The vaccines appear to be doing their job of reducing the worst-case outcome of the disease, making it unlikely – in our view – that new restrictions will occur in the U.S. and other countries with high vaccination rates.

The Fed’s shift, and the rise of the Delta variant, may together explain why some market participants are worried about a growth scare – meaning a downshift in GDP growth – which is causing an unwinding of so-called reflation trades.

What Does it All Mean for Goals-Based Plans?

This may end up being a tempest in the bond market tea cup. In Horizon Investments’ view, markets are digesting the meaning of several recent events, but the big picture has yet to change. The stock market, for example, was at record highs this week. Despite the unclear reasons for the bond market move, investors don’t appear to be concerned about the prospects for earnings and revenue growth.

Horizon believes it may be a good idea for financial advisors and their clients to not make any major adjustments if they have a diversified portfolio. In our view, the recovery of the U.S. economy should continue, the jump in inflation still appears to be temporary and the Federal Reserve – along with other major central banks – is not yet reducing their highly stimulative monetary policy stance. Taken together, we still believe the long-term economic path is for moderate GDP growth and tame inflation: conditions that are a favorable backdrop for market valuations.