Some assets may have rallied too far, too fast

Investors have breathed multiple sighs of relief in recent weeks as the Trump administration has dialed back its extreme tariff rates on China and other countries. In addition, first-quarter earnings were better, overall, than many expected given the quarter’s uncertainty.

As a result, there has been a rally in risk assets such as equities and high-yield bonds.

But have these assets come too far, too fast?

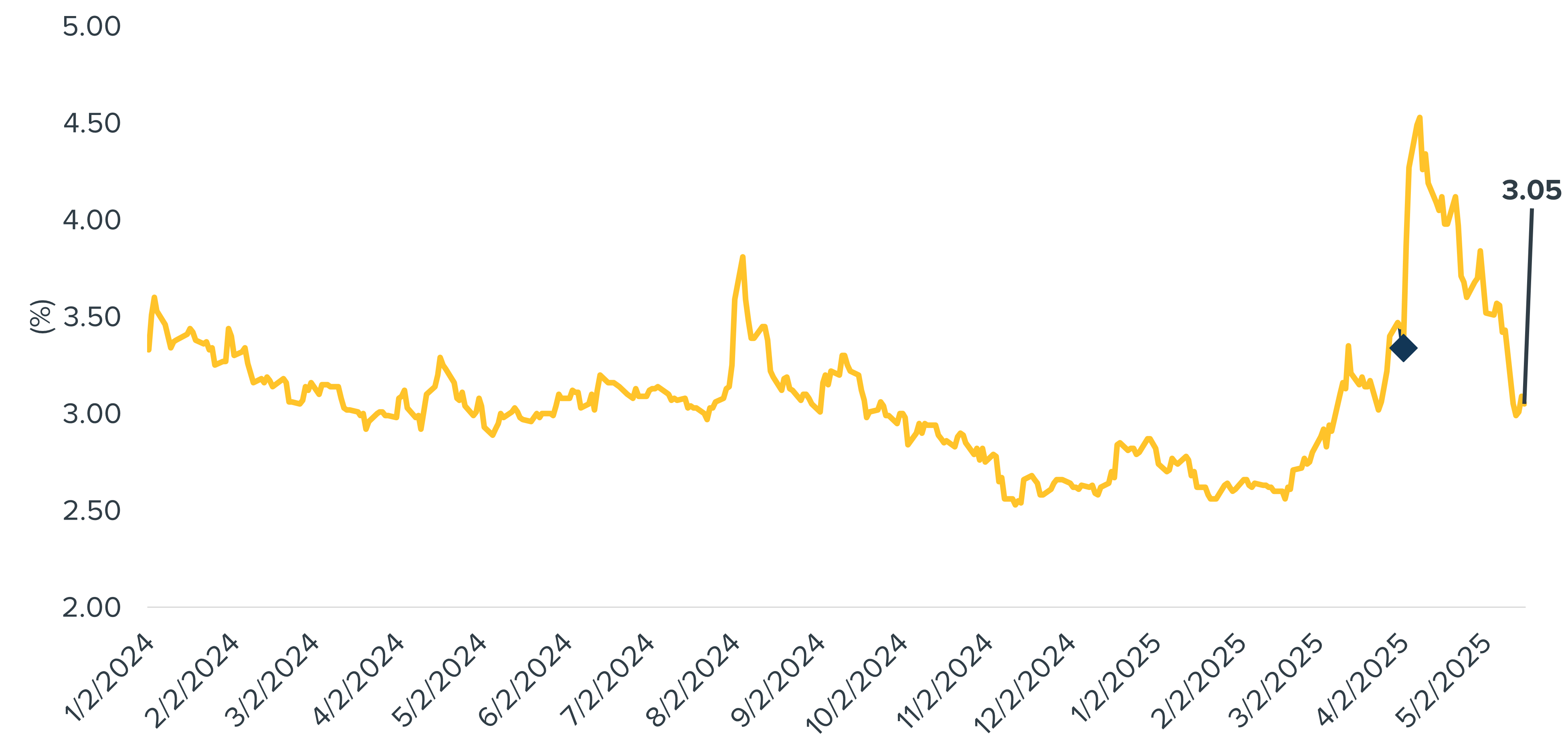

Consider the spread between high-yield bonds and comparable duration low-risk U.S. Treasury bonds. Simply, this spread acts as a market-based gauge of credit risk and economic sentiment. As seen in the chart, high-yield bonds are currently yielding 305 basis points more than Treasuries. That’s significantly lower than the 334-basis-point spread seen right before Trump surprised investors with his Liberation Day tariffs in early April (indicated by the red diamond in the chart).

Spread Between High-Yield Bonds and Comparable Duration Treasury Bonds

(as measured by Bloomberg US Corporate High Yield Average OAS Index)

Source: Bloomberg, calculations by Horizon Investments, data as of 05/16/25.

The upshot: Today’s market sees junk bonds as relatively less risky than before Trump started the trade war. While they may be right, there’s no question that much uncertainty remains about where tariffs may go from here, how the U.S. and various countries will reach new trade deals, inflation, consumer spending, and economic growth.

Given those and other question marks, we believe many goals-based investors should consider adopting strategies that allow them to participate in potential market gains going forward and mitigate the risk to their portfolios from sharp downturns brought on by more surprises. Because markets have rallied, investors should review their risk tolerance appetite following the recent volatility and reconsider their impulse to abandon risk mitigation strategies.