Over the summer months, Horizon conducted the firm’s first annual Advisor Sentiment Survey to gauge opinions and expectations around the current market, interest rates, asset classes, and the overall nature of client interaction this year. The results were informative, showing signs of optimism from advisors across equities, fixed-income, and alternative asset classes – and, as expected, based on broad consumer sentiment, showed that clients aren’t overly fearful in the current market.

Equities

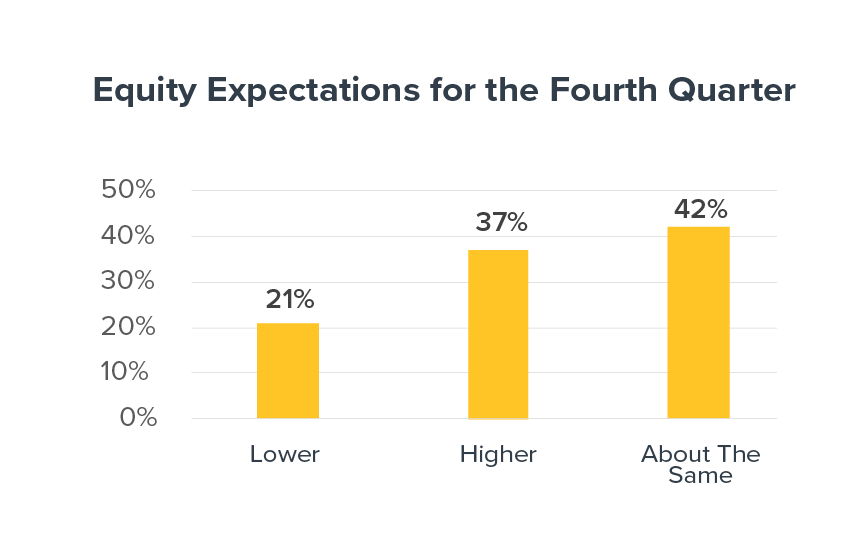

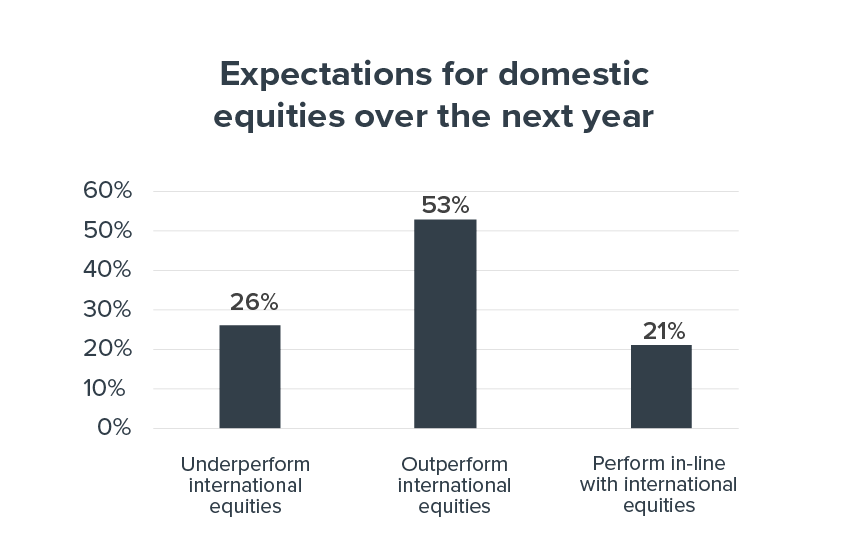

Expectations for equities as we move into the fourth quarter of 2023 are mixed, with 37% of respondents expecting equities to be higher towards the end of the year, 42% responding “about the same,” and 21% expecting equities to move lower. When asked about the view twelve months out, home bias appeared strong, with 53% of respondents expecting domestic equities to outperform international equities, 26% expecting domestic stocks to underperform, and 21% expecting to see parity between the two.

Source: Horizon Investments Advisor Sentiment Survey 1

Fixed Income

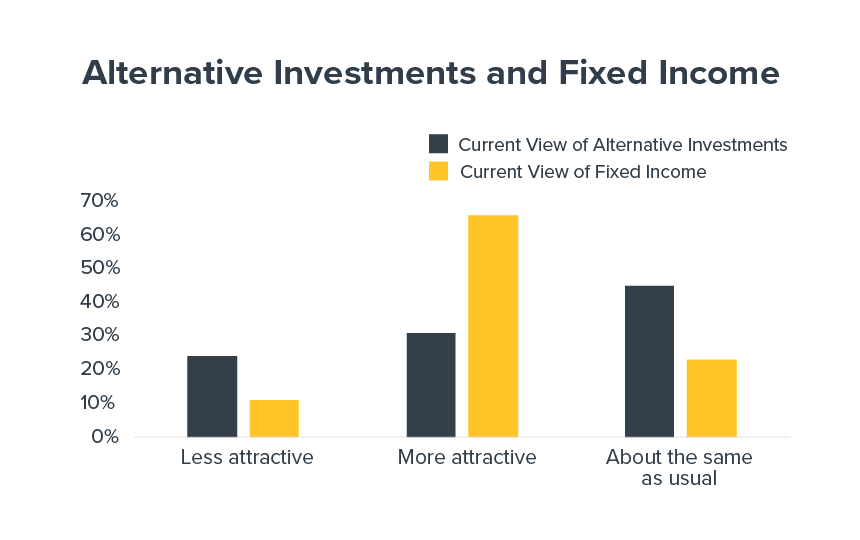

Sentiment around fixed income was resoundingly positive, with 66% of survey takers viewing the asset class as “more attractive” in the current market. Only 11% viewed fixed income as less attractive, leaving 23% of respondents feeling neutral.

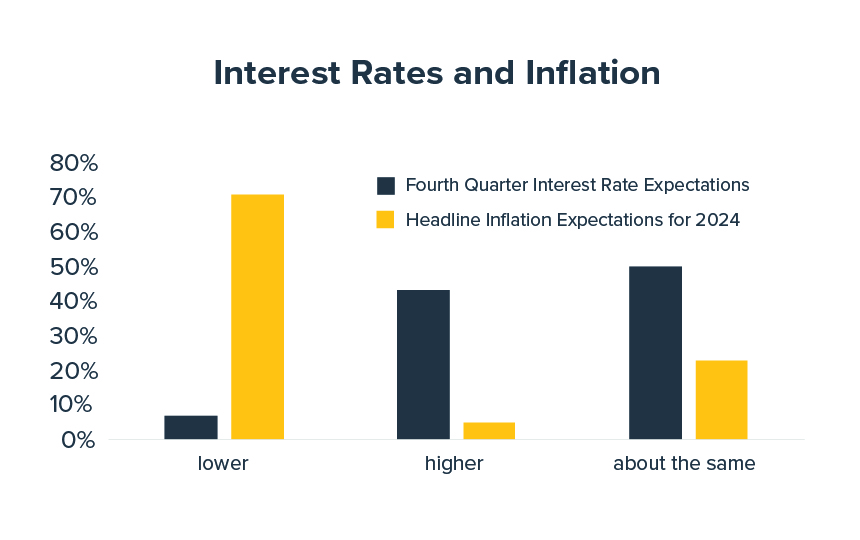

The advisors we surveyed expect to either see interest rates remaining the same as we move through the fall or moving higher. In all fairness, this question is a moving target closely tied to Fed messaging from month to month, and advisors surveyed today would most likely expect rates to stay the same.

Considering inflation, while 93% of respondents expect rates to stay the same or move higher soon, 71% expect headline inflation to move lower over the next year.

Alternative Asset Classes

Thoughts around alternative investment products were relatively neutral. Forty-five percent answered, “about the same as usual,” with the remaining advisors more closely split between less attractive and more attractive; 24% and 31%, respectively.

Practice Management

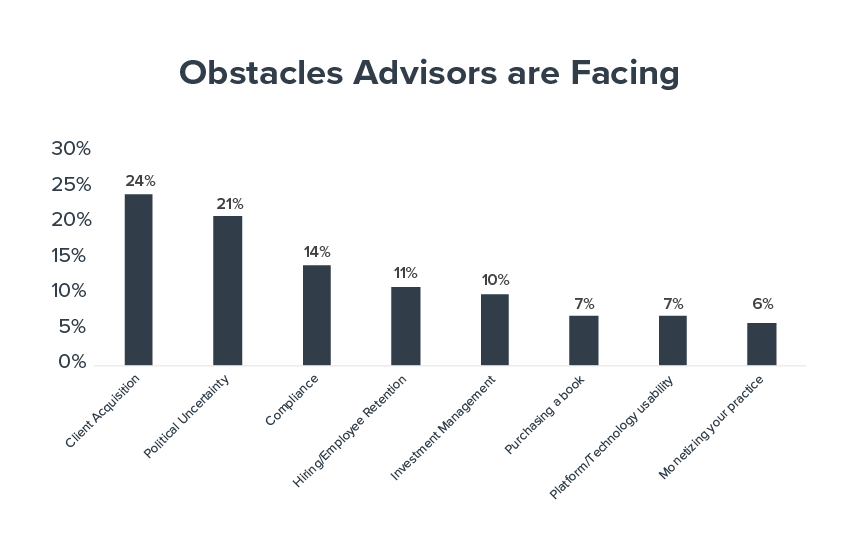

We also asked advisors what obstacles they face in their practice and current trends they find attractive; client acquisition, political uncertainty, and compliance were the top three concerns from the 468 respondents. They were less concerned about growing through acquisition, technological enhancements, and monetizing their practices.

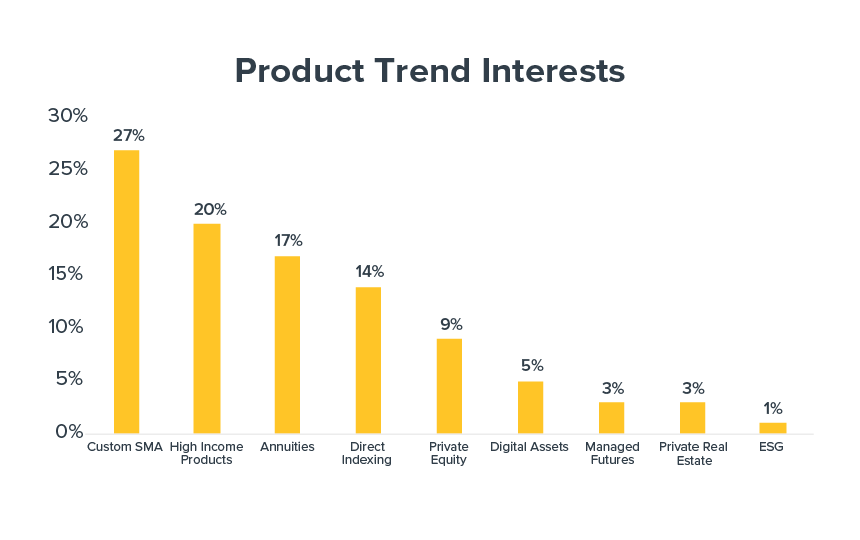

Trend-wise, separately managed accounts (SMAs) appear to be the most interesting product offering, with nearly half of respondents listing Custom SMA solutions and direct indexing as most attractive, followed by high-income products, annuities, and private equity. Less than 1% showed interest in ESG investments.

Source: Horizon Investments Advisor Sentiment Survey 1

Client Behavior & Market Sentiment

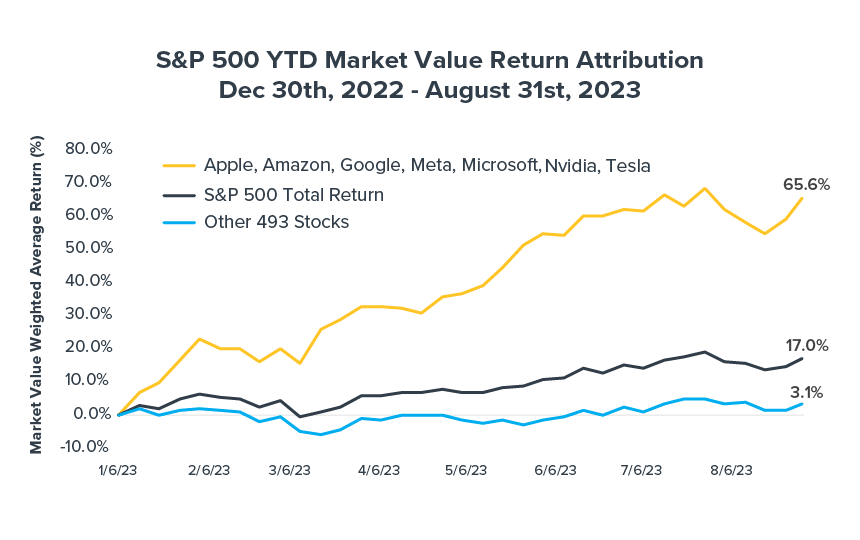

Most survey takers find communications with clients to be business as usual this year, and a third find prospecting even easier than in past years, likely due to overall market sentiment rising after a rough ride through 2022. Economic data has continued to surprise on the upside, and equities appear to be recovering, with the S&P 500 up 17.40% year to date through the end of August. However, we assume the 42% of advisors who expect equities to remain the same through year-end are keeping in mind that while the S&P 500 continued its winning streak through the summer months, showing the best performance through the first seven months of a calendar year since 1997, seven stocks (Apple, Amazon, Google, Meta, Microsoft, Nvidia, and Tesla) continue to pull far ahead of the remaining 493 stocks in the index, which collectively returned only 3.1% through August 31. The “Magnificent 7” returned a whopping 65.6% for the same period.

Source: Horizon Investments Advisor Sentiment Survey

This is not a recommendation to buy or sell any security. It is not possible to invest directly in an index.

The index moved below its 50-day moving average for the first time since March in mid-August, signaling the potential for turbulence ahead. That aligns with the 63% of respondents who see equities moving lower or staying the same as we close out the year.

The most significant pain point for investors this year has likely been fixed income. Since the end of the first quarter, broad bonds were down -1.55% through August, due to higher bond yields rising from their year-to-date lows (2-year Treasury up 43 basis points, and the 10-year Treasury yield higher by 24 basis points).

Changes Expected for the Remainder of the Year

Economically, we’ve seen many positives this year, with over three million more people employed and real GDP expanding by 2.6% over the last four quarters. Year-over-year Inflation fell by 5.4 percentage points to 3.7% as of August 31st, 2023, from the high of 9.1% in June of 2022 as measured by the consumer price index. However, as we watch oil prices hit their highest point in 10 months and consumer prices increase (jumping 0.6% in August), market sentiment has the potential to shift. Higher fuel prices will hit consumer pockets in more ways than filling up their cars, and rekindling inflation will be on investors’ minds.

Conclusion

As a modern goals-based investment manager, we aim to help financial advisors and their clients achieve their financial goals. We prioritize keeping a close eye on industry trends and monitoring advisors’ thoughts and concerns, seeking to improve the investing experience across market environments.

It was a pleasure to connect with many of the advisors we work with daily to discuss their views on the market, economy, practice management, and overall expectations for their business. We look forward to continuing to gather feedback from advisors periodically and making our findings available for years to come.

Disclosure

The index moved below its 50-day moving average for the first time since March in mid-August, signaling the potential for turbulence ahead. That aligns with the 63% of respondents who see equities moving lower or staying the same as we close out the year.

The most significant pain point for investors this year has likely been fixed income. Since the end of the first quarter, broad bonds were down -1.55% through August, due to higher bond yields rising from their year-to-date lows (2-year Treasury up 43 basis points, and the 10-year Treasury yield higher by 24 basis points).

Changes Expected for the Remainder of the Year

Economically, we’ve seen many positives this year, with over three million more people employed and real GDP expanding by 2.6% over the last four quarters. Year-over-year Inflation fell by 5.4 percentage points to 3.7% as of August 31st, 2023, from the high of 9.1% in June of 2022 as measured by the consumer price index. However, as we watch oil prices hit their highest point in 10 months and consumer prices increase (jumping 0.6% in August), market sentiment has the potential to shift. Higher fuel prices will hit consumer pockets in more ways than filling up their cars, and rekindling inflation will be on investors’ minds.

Conclusion

As a modern goals-based investment manager, we aim to help financial advisors and their clients achieve their financial goals. We prioritize keeping a close eye on industry trends and monitoring advisors’ thoughts and concerns, seeking to improve the investing experience across market environments.

It was a pleasure to connect with many of the advisors we work with daily to discuss their views on the market, economy, practice management, and overall expectations for their business. We look forward to continuing to gather feedback from advisors periodically and making our findings available for years to come.