GDP growth over the past three months may have been huuuuuge.

Third-quarter GDP growth could be a monster.

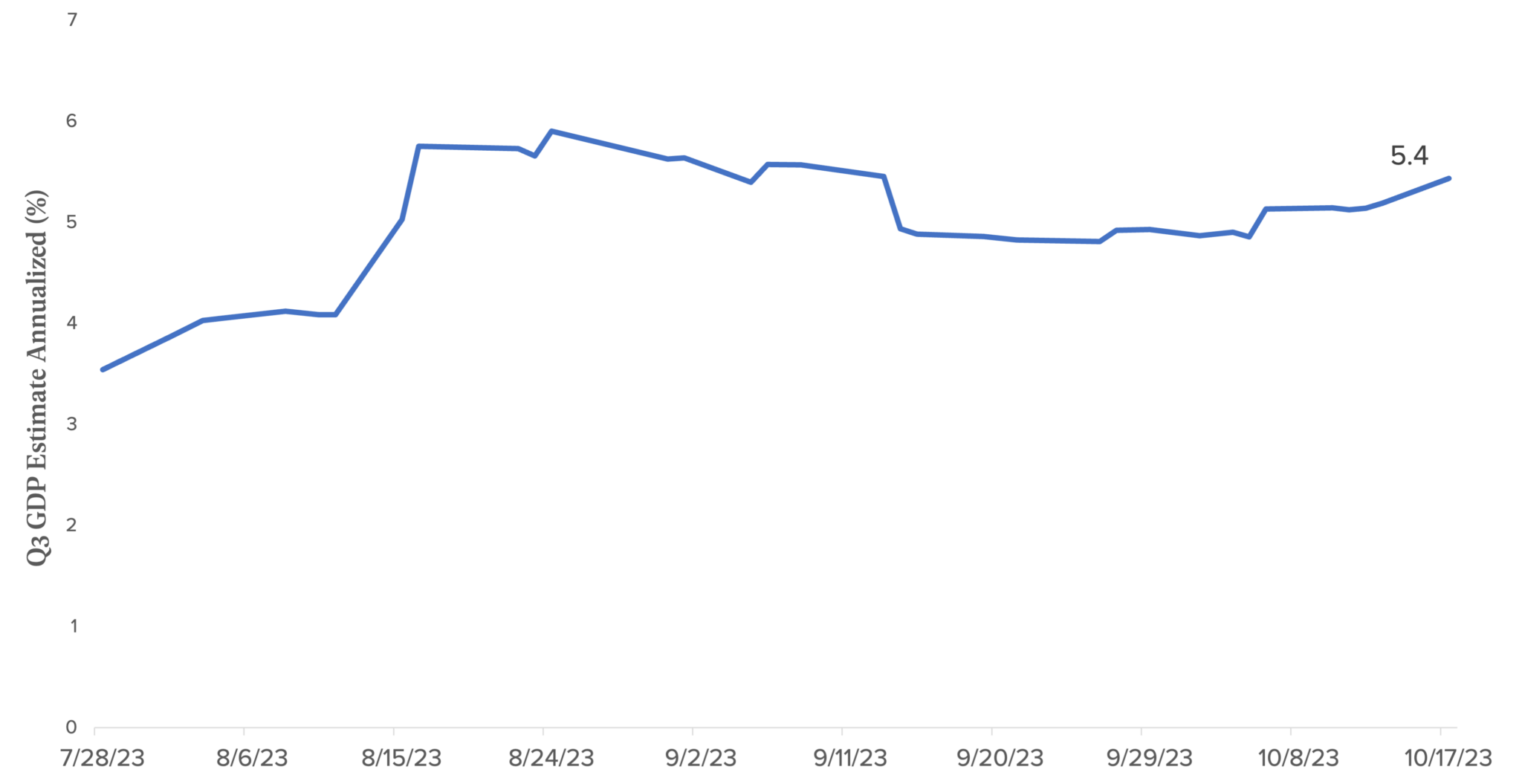

True, it’ll be a few weeks before we get the first official word on how fast the U.S. economy expanded from July through September. But currently, the Federal Reserve Bank of Atlanta’s forecasting model—GDPNow—is calling for a whopping 5.4% surge for the quarter (see the chart).

The Atlanta Fed’s model serves as a running estimate of real GDP growth (seasonally adjusted annual rate) based on available economic data that’s been released. The model is regularly updated as new numbers come out—and as of now, most third-quarter data is public knowledge.

In short, that 5.4% estimate has lots of quantitative support behind it.

If the GDPNow model is accurate, it will represent a remarkable jump from the 2.1% growth rate in the second quarter and the 2.2% rise seen during the first three months of the year. We believe this expected pickup in economic activity may also explain a portion of the sharp increase in longer-term yields leaving the US 10-year at nearly 5%, while providing support at these levels and be constructive for third-quarter earnings.

The driver of this sanguine forecast is, not surprisingly, U.S. consumers—who have shown remarkable resilience and a willingness to keep spending despite rising interest rates. For example, actual personal spending data during the quarter accounts for half of GDPNow’s 5.4% estimate.

- Falling inflation is helping boost economic activity, with the consumer price index coming in at 3.7% in September (year over year), roughly in line with expectations and down from 6.4% back in January.

- Meanwhile, the job market is defying all odds—with employers adding nearly twice as many jobs in September as expected.

It’s important to note that GDPNow isn’t the only game in town and that other models suggest slower growth. For example, the New York Fed’s Nowcast is looking for 2.5% GDP growth for the quarter, while the median consensus of economic forecasters on Bloomberg is 3.0%.

We’ll know soon whether the GDPNow model is on target. But regardless, it’s clear that a strong consumer continues to add fuel to the U.S. economic engine.